Part I: UK XR Healthcare Market Assessment

Introduction

Extended Reality (XR) technologies, encompassing virtual reality (VR), augmented reality (AR), mixed reality (MR), and related immersive systems, are increasingly being explored across the UK for applications in healthcare, education, and research [1]. While early adoption was often concentrated in specialist centres and research projects, the pace of implementation has accelerated in recent years, particularly following the COVID-19 pandemic, which prompted rapid digital innovation in service delivery and training [8]. Despite this growth, there remains limited up-to-date evidence on the extent, nature, and maturity of XR adoption across different sectors, including the NHS, universities, and private companies. Understanding where and how XR is currently being used, as well as the challenges and opportunities faced, is imperative for identifying good practice, supporting investment, and informing policy and regulation.

To address this evidence gap, Freedom of Information (FOI) requests and sector-specific surveys were conducted to capture a snapshot of XR deployment across the UK. Separate but comparable data collections targeted NHS Trusts in England, Health Boards in Scotland and Wales, and Trusts in Northern Ireland; UK universities; and private sector companies operating in the XR healthcare and mental health space. The findings presented in this report provide an analysis of responses received up until 1st September 2025.

This section focuses on NHS adoption of XR technologies, summarising the responses from Trusts in each country and highlighting key trends in uptake, areas of application, maturity of deployment, and supporting infrastructure such as laboratories and centres of excellence. The results provide an important baseline for understanding the current position of XR within the NHS, as well as insights into emerging patterns that may inform future roll-out and cross-sector collaboration.

NHS

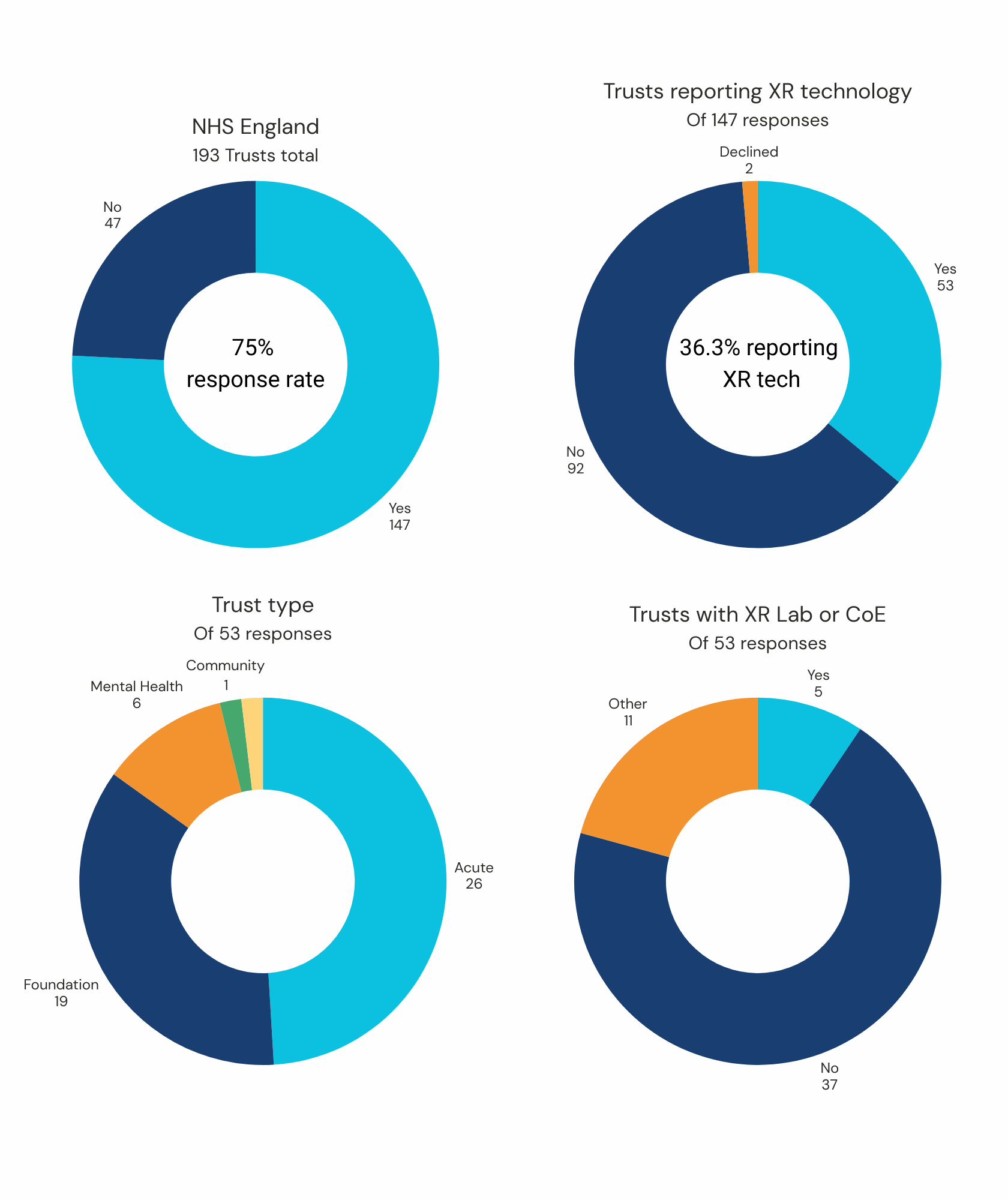

On the 19th June 2025, FOI requests were sent to all NHS Trusts in England with further requests sent to the Health Boards of Scotland and Wales and Trusts of Northern Ireland on the 10th July. As of the 1st September, 147 responses had been received from the 194 Trusts in England (75%) in addition to responses from all of the NHS Scotland and Wales Health Boards and four of the six Northern Ireland Health and Social Care Trusts.

England

Of the 147 responses received from Trusts in England, 53 reported having XR technology (36.3%) within their organisation with 92 reporting no XR technology and 2 declining to respond to the FOI requests, either due to the time limit associated with FOI requests or cybersecurity concerns.

Overview of Trusts

Of the 53 Trusts reporting XR technologies, 26 were Acute (Hospital) Trusts, 19 were Foundation Trusts, 6 were Mental Health Trusts, 1 was Community Health Trust and 1 was a Specialist/Integrated Trust. Furthermore, 5 Trusts reported having a dedicated Lab or Centre of Excellence (CoE) for XR technologies. 37 Trusts reported no Lab or CoE but 11 Trusts reported having teams, units, suites or communities within their Trust focused on XR technologies and one upcoming National Centre for Child Health Technology currently being built.

193 Trusts total • 75% response rate

Of 147 responses • 36% reporting XR

Of 53 responses

Of 53 responses

XR Adoption

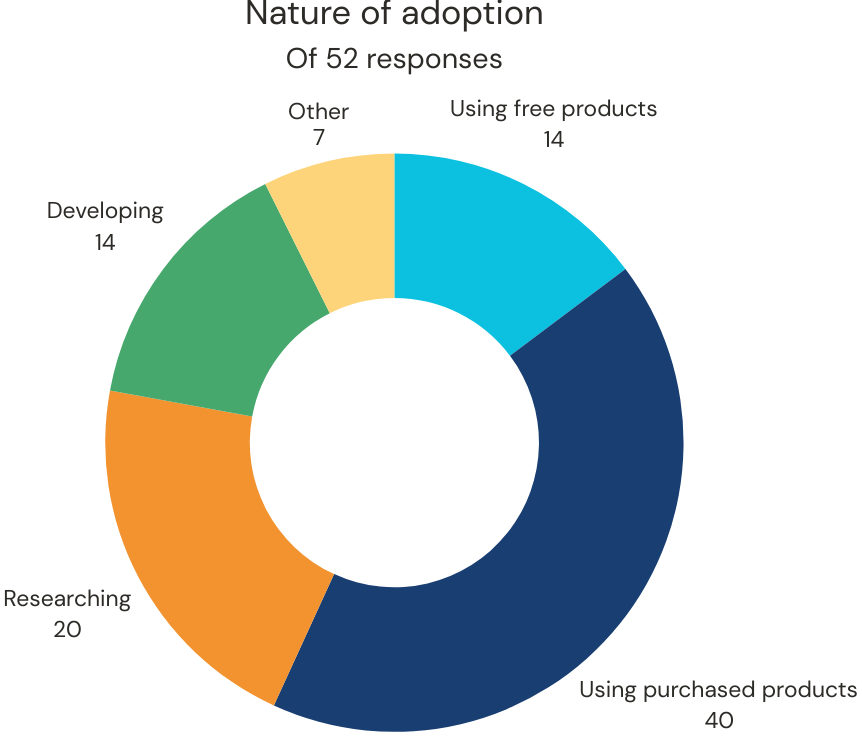

One Trust provided a partial response and therefore, the following data accounts for 52 Trust responses. Trusts varied in their adoption of XR technologies, most commonly reporting the use of purchased products, however the FOI request allowed respondents to select all appropriate categories of adoption. As a result, 14 reported using free XR products, 40 reported using purchased products, 20 reported researching technologies and 14 reported developing XR technology. A further 7 selected ‘other’ with one clarifying that the Trust was using an XR technology as part of a trial.

Maturity

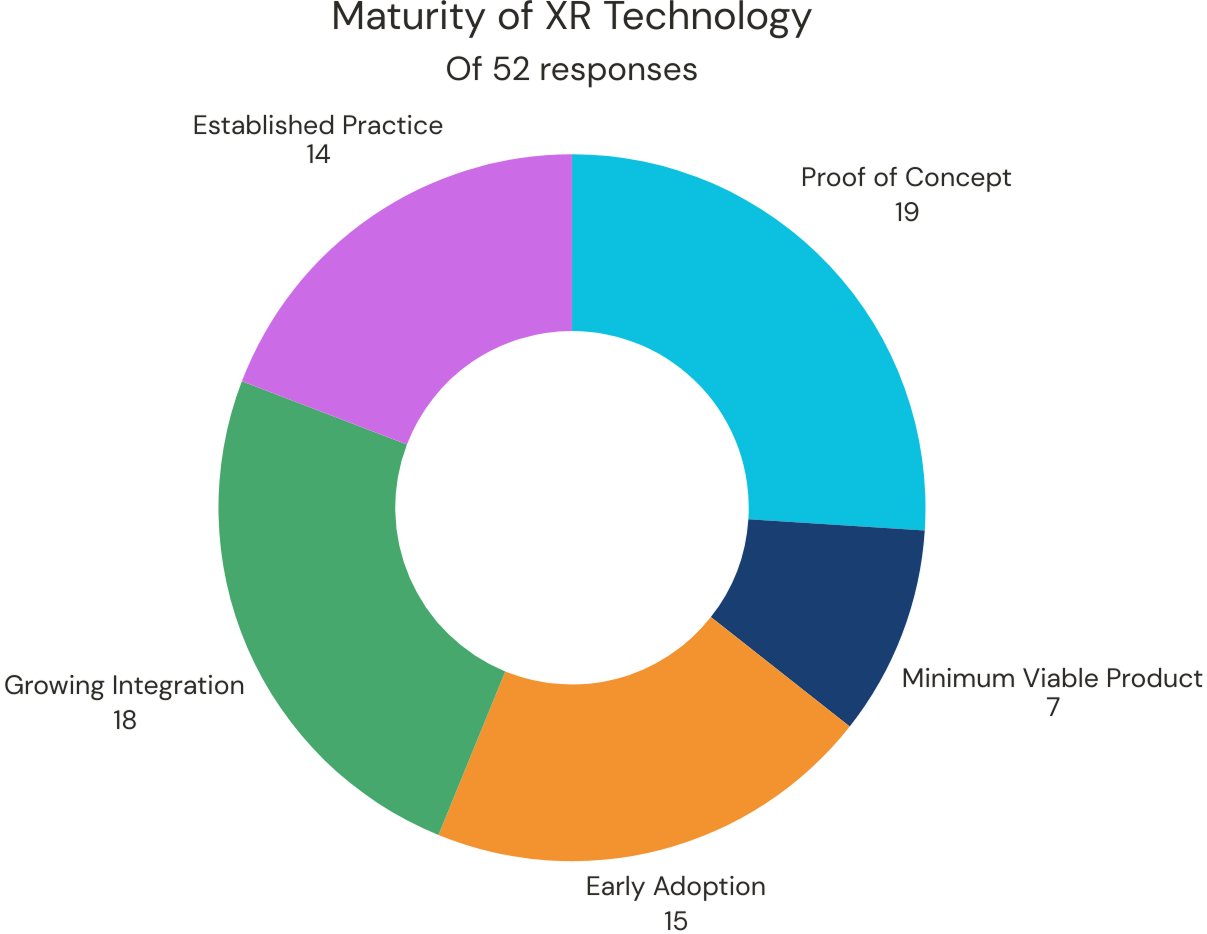

These technologies varied in their maturity with 19 being Proof of Concept and 14 being Established Practice, with 7 being a Minimum Viable Product, 15 being in early adoption and 18 growing integration.

Of 52 responses

Of 52 responses

Purpose

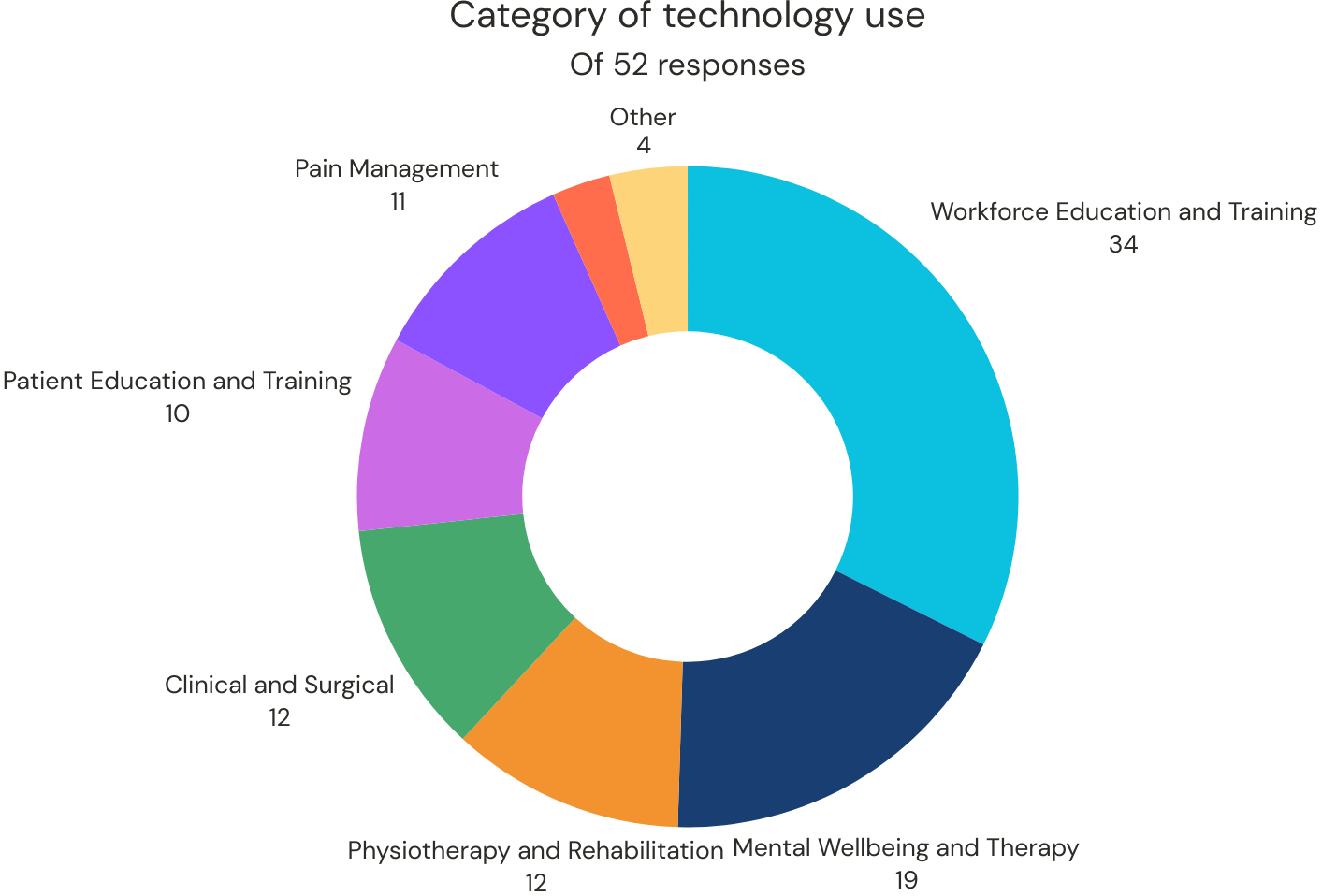

Of the technologies being reported, the most common category was technology being used for Workforce Education and Training (n=34). This is followed by Mental Wellbeing and Therapy (n=19), Physiotherapy and Rehabilitation (n=12), Clinical and Surgical (n=12), Patient Education and Training (n=10), Pain Management (n=11) and Healthy Lifestyle and Fitness (n=3). 4 selected ‘Other’.

Of 52 responses

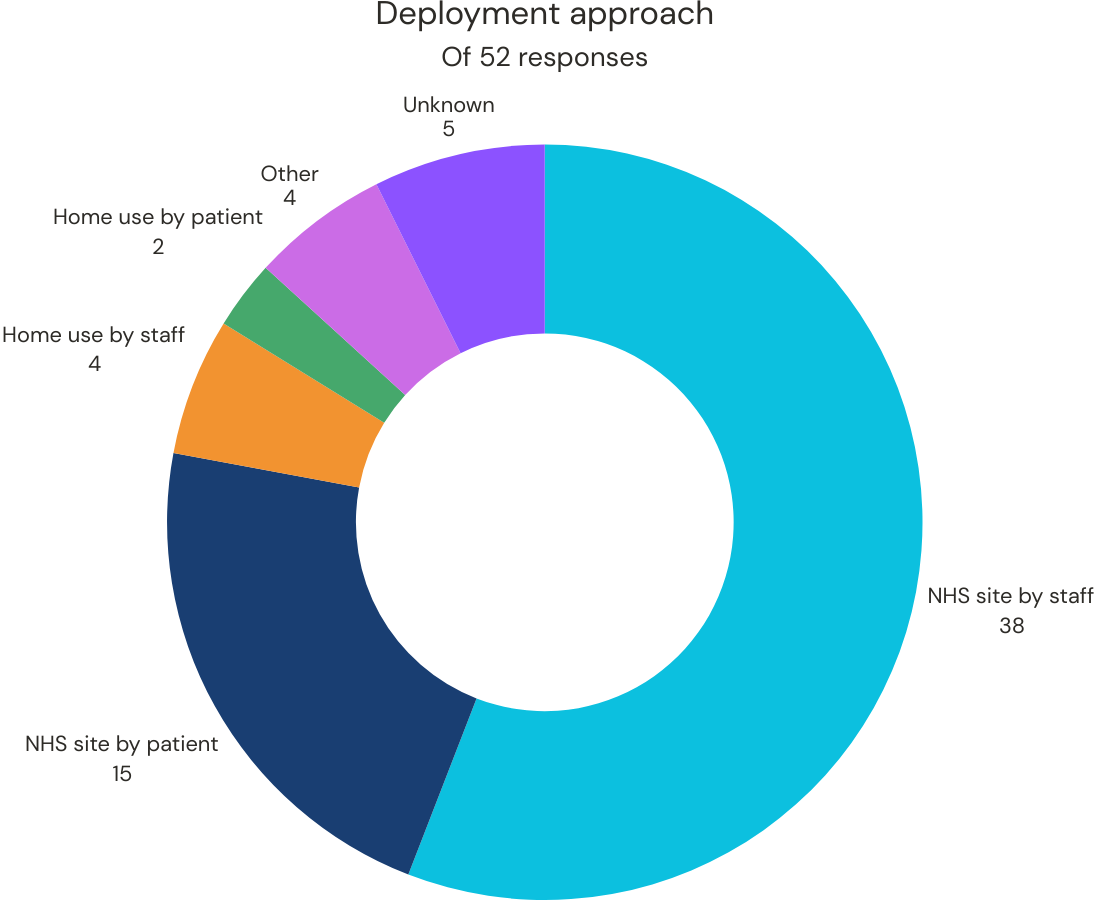

Distribution and deployment

When asked about how the technology is distributed, the most common answer was that XR technology is used at NHS sites by staff members (n=20), followed by being used at NHS sites by patients (n=3), home use by staff (n=2) and home use by patients (n=1).

Of 52 responses

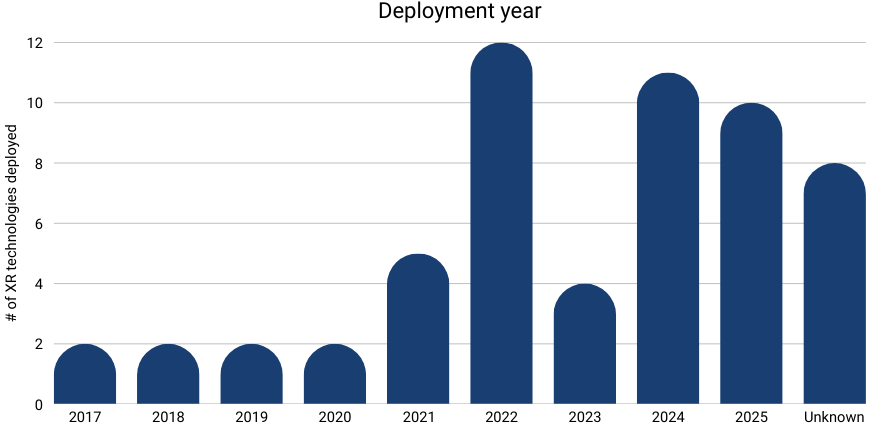

Deployment of XR in the NHS has steadily increased over the years, with 2022 being the peak deployment year (12 technologies) so far but 2025 statistics already show to be approaching this number (10), showing an encouraging trend. This upward trend of deployment in NHS England demonstrates the impact that the Covid-19 pandemic and NHS Long Term Plans may have had in encouraging the adoption of these technologies into service delivery.

Types of XR

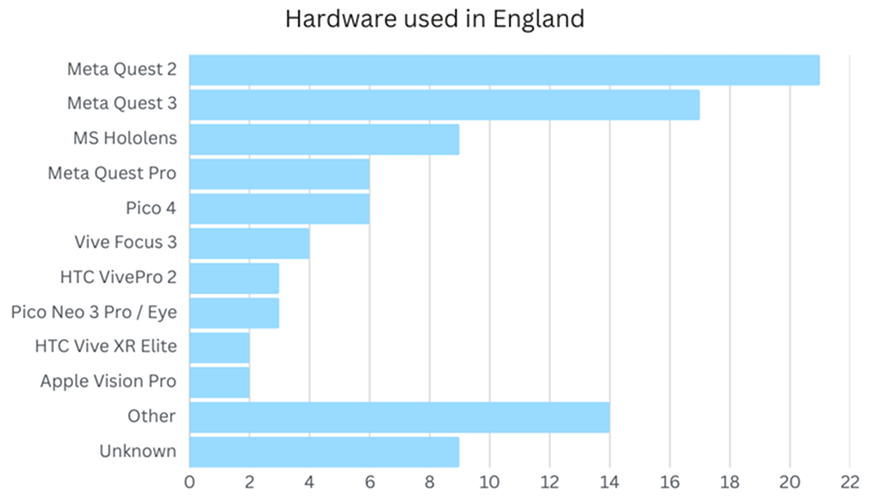

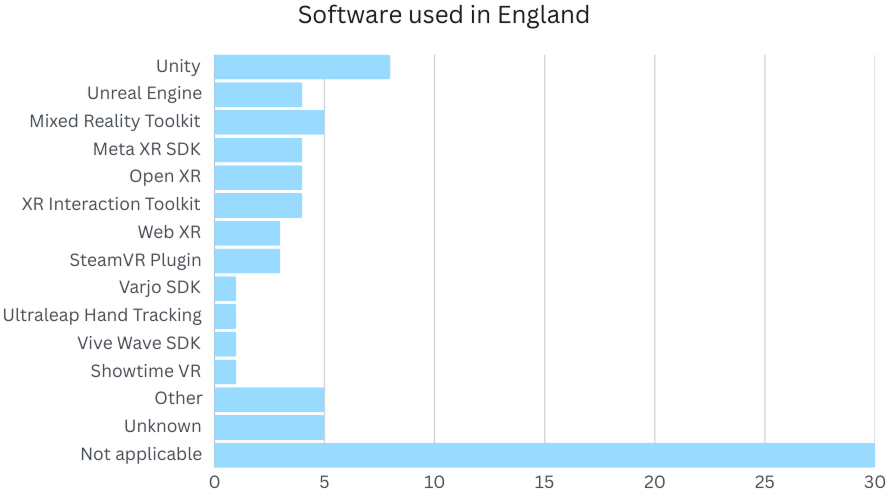

Meta products were the most commonly reported XR hardware being used by Trusts, followed by the Microsoft Hololens, Pico products and HTC. Those Trusts that selected ‘other’ technologies included technologies such as Cave Automatic Virtual Environments (CAVEs). ‘Unknown’ indicates Trusts were unable to answer or not aware of which hardware is being used. Additionally, many Trusts were unable to answer which software was being used to develop new XR technologies or this was ‘not applicable’ to those not developing XR. However, Unity was marginally the most popular.

Scotland

All of the 14 Health Boards of NHS Scotland replied to the FOI requests for this project. Of these 14 Health Boards, 4 reported having XR technology within their organisation, with the remaining 9 reporting no XR technology being used and 1 Health Board declining the request. The Health Boards reporting XR technology are as follows:

- NHS Fife

- NHS Forth Valley

- NHS Greater Glasgow & Clyde (NHSGGC)

- NHS Highland

None of these Health Boards reported having a dedicated Lab or Centre of Excellence for XR technology, but three reported using purchased XR products and the other reported to be conducting research into XR technologies for health.

When asked which products are being adopted by these Health Boards, some included a list of hardware and headsets such as the Meta Quest and Vision Pro headsets but the following products and their uses were also reported:

- Sim X is a VR simulation system used in medical education and training to reinforce critical thinking and clinical decision-making by simulating patient conditions.

- PeriVision for VR-based visual function testing and home/near-patient glaucoma monitoring.

- Healthy Mind for immersion to combine VR technology, medical hypnosis and advanced therapeutic principles to alleviate pain and anxiety.

- Brain Lab to bring 3D perspectives into functional neurosurgery case reviews.

Oxford Medical Simulation and other teaching pilots were also reported. Of these reported technologies and their level of maturity, one was Proof of Concept, two were in Early Adoption, one was Growing Integration and one was Unknown. These Health Boards were also asked which categories in which these technologies were being used:

- NHS Fife: Clinical and Surgical & Workforce Education and Training

- NHS Forth Valley: Clinical and Surgical, Patient Education and Training & Workforce Education and Training

- NHS Greater Glasgow & Clyde: Clinical and Surgical

- NHS Highland: Mental Wellbeing and Therapy, Pain Management & Workforce Education and Training.

All of these technologies were being used on NHS sites only, three with staff and one with patients. One was reportedly deployed in 2024, another in 2025 with the others either not being deployed yet or unknown. Health Boards reportedly used Apple Vision Pro and Meta Quest Pro (1), Meta Quest 3 (1), Pico Neo 3 Pro / Eye and Meta Quest 2 (1) headsets for their hardware with one reporting ‘not applicable’ and all Health Boards were unable to answer which software was being used.

Wales

All of the 7 Health Boards of NHS Wales replied to the FOI requests for this project. Of these 7 Health Boards, 3 reported having XR technology within their organisation, with the remaining 4 reporting no XR technology. The Health Boards reporting XR technology are as follows:

- Aneurin Bevan University Health Board

- Cwm Taf Morgannwg University Health Board

- Powys Teaching Health Board

None of these Health Boards reported having a dedicated Lab or Centre of Excellence for XR technology, but two reported using purchased XR products and the other reported to be using purchased products and conducting research into XR technologies.

When asked which products are being adopted by these Health Boards, some included a list of hardware and headsets such as the Meta Quest 3 and Microsoft Hololens headsets but one Health Board also reported the use of the commercial product, DR.VR. This product provides four different types of content: distraction, instructional, relaxation course (8 relaxation and mindfulness meditation sessions) and games and patients can choose which content they would like to access.

Of these reported technologies and their level of maturity, one was Proof of Concept, one was Growing Integration and one was reported as ‘other’. These NHS Bodies were also asked which categories in which these technologies were being used:

- Aneurin Bevan University Health Board: Mental Wellbeing and Therapy & Healthy Lifestyle and Fitness

- Cwm Taf Morgannwg University Health Board: Mental Wellbeing and Therapy

- Powys Teaching Health Board: Clinical and Surgical

Two of the NHS Bodies reported that the XR technology is used on NHS sites only by patients and staff with the other being used at home by staff. One was reportedly deployed in 2021, another in 2022 and the final being deployed in 2024. NHS Bodies reportedly used the Meta Quest 3 (1) and Microsoft Hololens (1) headsets for their hardware with one reporting use of only the DR.VR headset and software. The remaining two NHS Bodies said the question on which software was being used was ‘not applicable’, suggesting it is not being used for development at all.

Northern Ireland

Freedom of Information requests were also sent to the 6 Health and Social Care Trusts of Northern Ireland, to which 4 responses. 2 of these Trusts reported using XR technology: Northern Health and Social Care Trust (NHSC) and Southern Health & Social Care Trust (SHSC). Neither Trust has a dedicated XR Lab or Centre for Excellence.

NHSC are reportedly using purchased products and also researching and developing XR technologies. For example, they are using Oculus Quest 3 headsets to create personalised immersive environments for use in exposure therapy for trauma and PTSD. Currently considered as being proof of concept, it was first deployed in 2022 for Mental Wellbeing and Therapy at NHS sites by staff and patients.

Meanwhile, SHSC uses purchased products but withheld aspects of information for cybersecurity reasons, but uses XR technology for virtual walk-throughs for patients prior to appointment attendance as part of patient familiarisation and anxiety prevention measures and for staff training for specialist work area walk-throughs. This was deployed in 2023 and is considered to be in early adoption stages in NHS sites. SHSC declined to say which hardware and software is being used by the Trust.

Universities

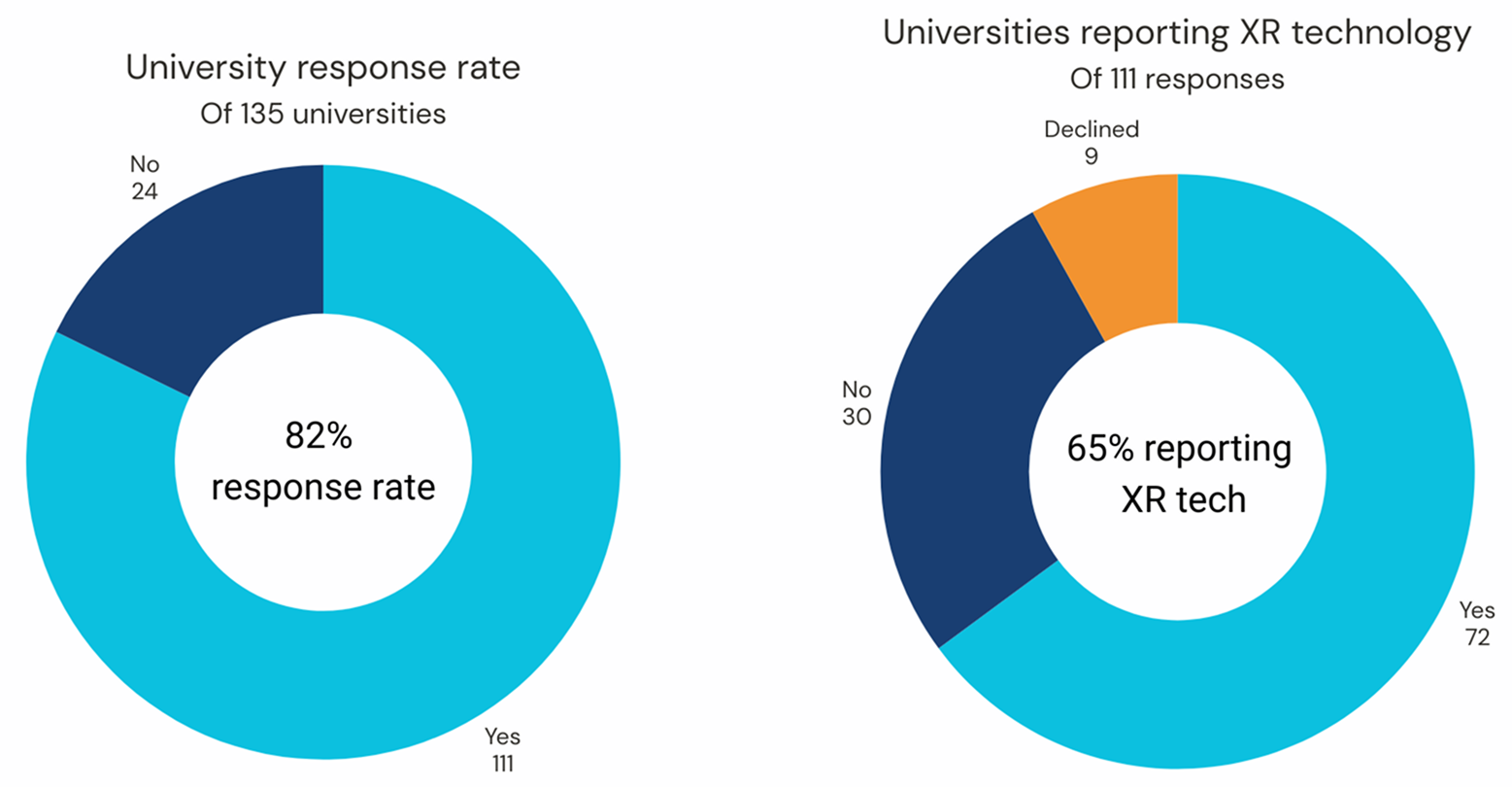

On the 19th June 2025, FOI requests were sent to all 135 registered universities in the UK. By the 1st September, 111 responses had been received (82%). Of these 111 responses, 72 universities reported using XR technology (65%) within their organisation with 30 reporting none and 9 declining to respond to the request. However, there were two separate joint responses, meaning 70 responses will be reported hereafter.

Of 135 universities • 82% response rate

Of 111 responses • 65% reporting XR

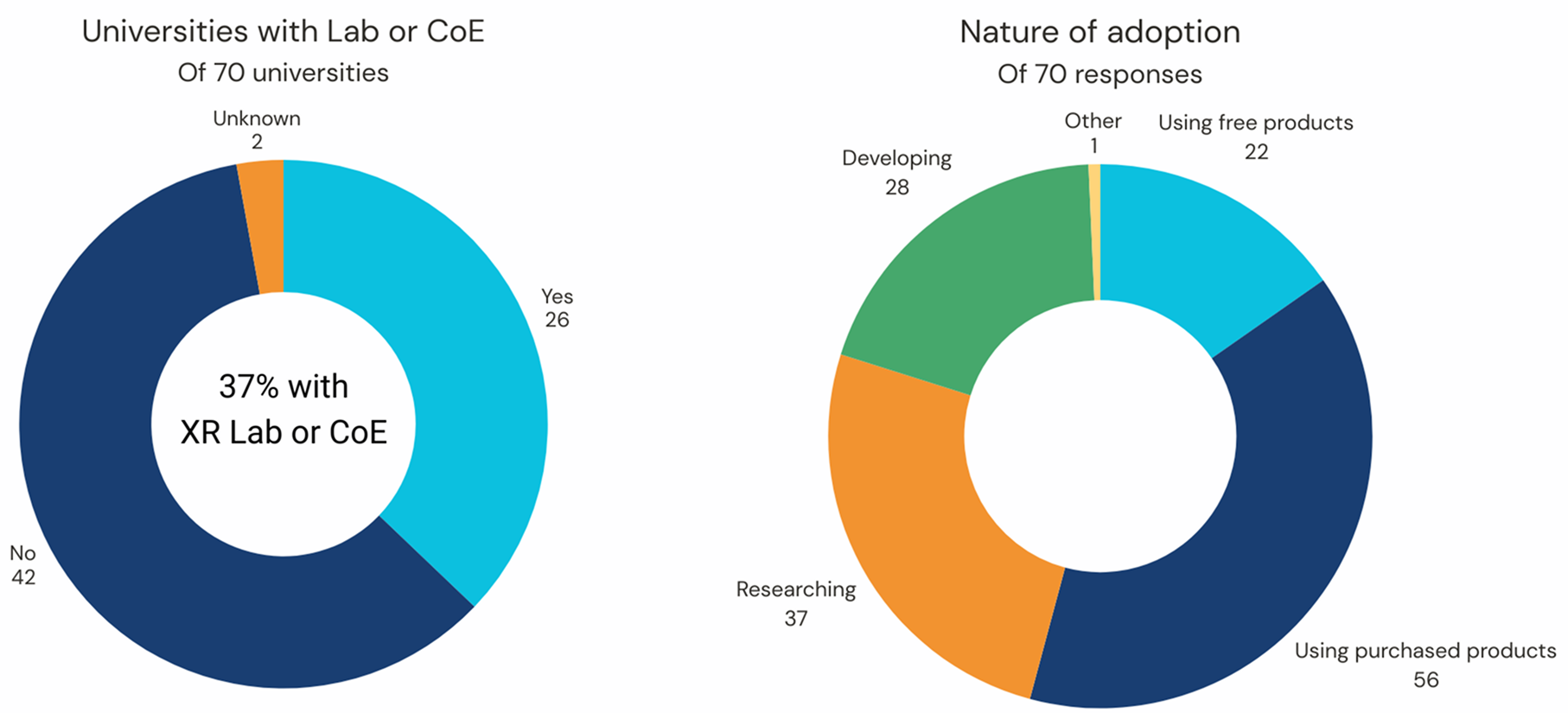

Of the 70 universities reporting that they have or use XR technology, 26 of these universities have a dedicated Lab or CoE for XR technology. A further 42 answered no but 10 of these reported having research groups, stimulation facilities or dedicated areas on campus for XR use or research and 2 selected ‘unknown’.

Of 70 universities • 37% have lab/CoE

Of 70 responses

Universities had a more even split between their nature of adoption for XR technology, but using purchased products was still most common (38.9%) and respondents were allowed to select all appropriate options. As a result, 22 reported using free XR products, 56 reported using purchased products, 37 reported researching technologies, 28 reported developing XR technology and 1 selected ‘other’.

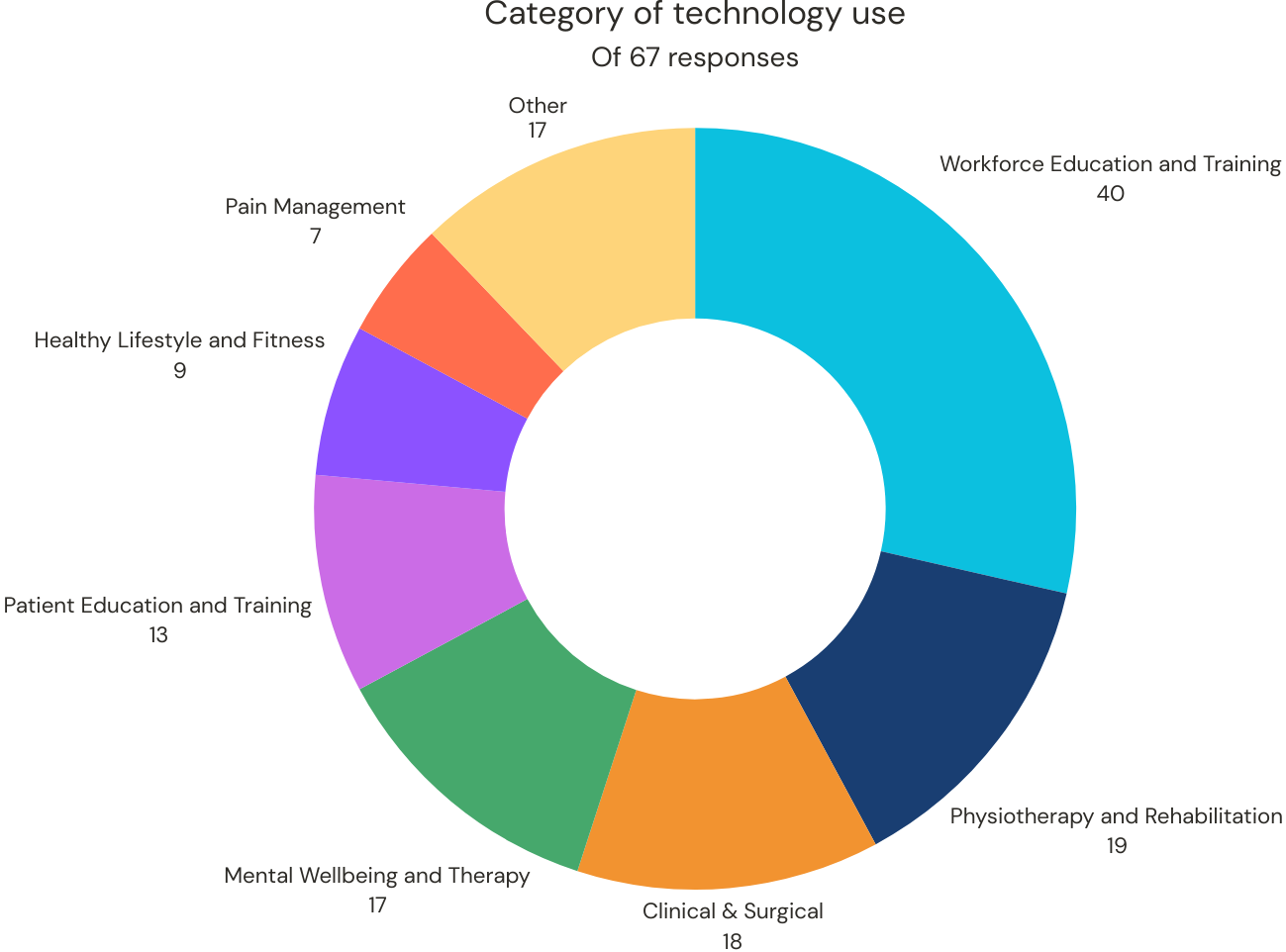

3 of the 70 respondents declined to answer further questions, therefore 67 responses will be reported hereafter. Similarly to the NHS responses, XR technology was most used, researched or developed for Workforce Education and Training (n=40). The next most common categories are Physiotherapy and Rehabilitation (n=19), Clinical and Surgical (n=18), Mental Wellbeing and Therapy (n=17), Patient Education and Training (n=13), Healthy Lifestyle and Fitness (n=9) then Pain Management (n=7). An additional 17 selected ‘other’, identifying that XR technology is used for student education and training which is one of the key differences between deployment in NHS settings versus use within university settings.

Of 67 responses

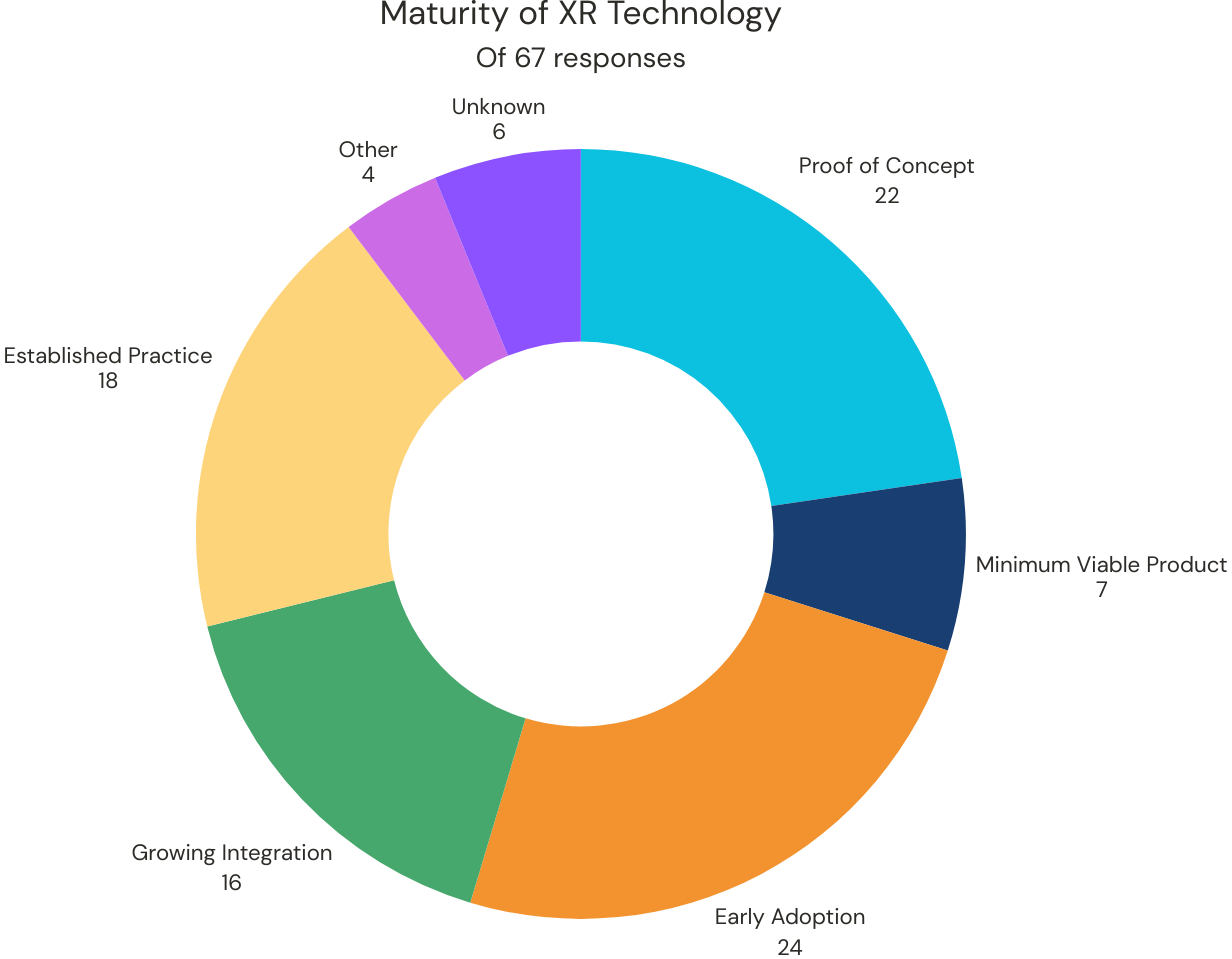

There was considerable variability in the maturity of the reported technology: 22 were Proof of Concept, 7 were Minimum Viable Products, 24 were in early adoption, 16 were growing in integration, 18 were established in practice in the organisations with another 6 being unknown and 4 ‘other’.

Of 67 responses

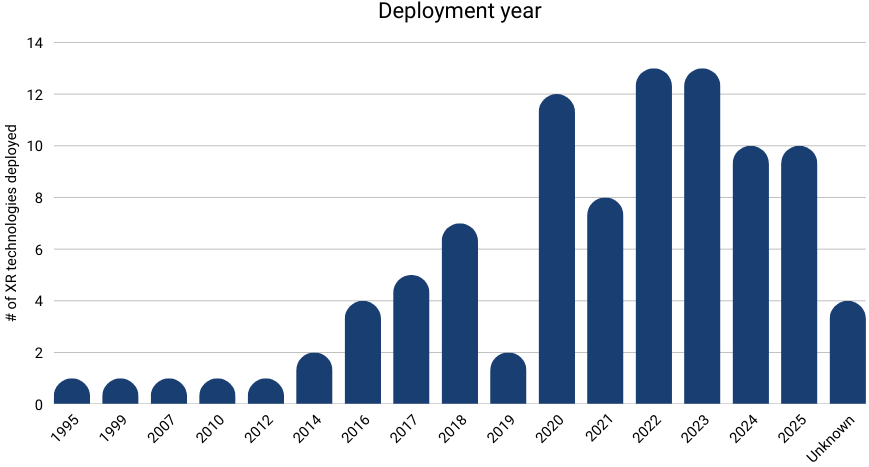

Compared to the NHS, XR technologies were being researched, developed and deployed in universities considerably earlier. Some reported technologies were being researched and deployed earlier than 2020, with XR research groups dating back to 1995 with some clarifying that research began before some technologies were formally deployed and available. Technologies were most commonly deployed during and following 2020, the year the pandemic started, with levels remaining steady thereafter. 4 reported the deployment date as ‘unknown’.

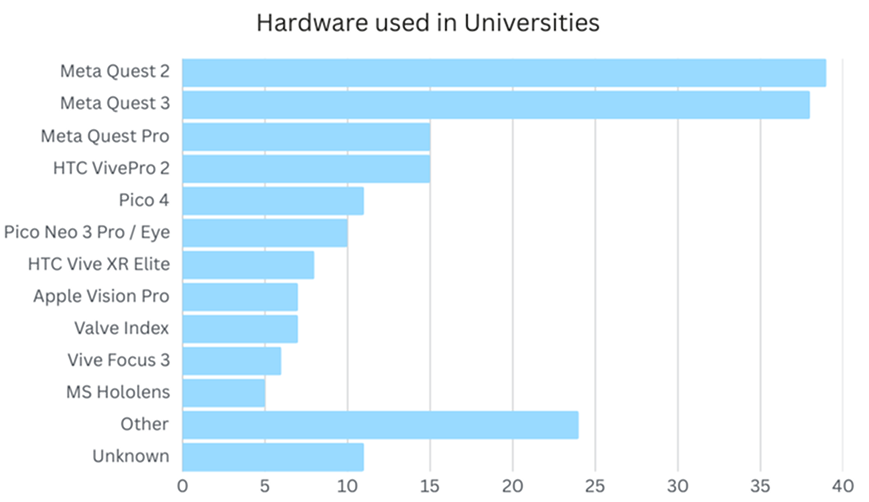

Universities also reported a significantly higher number of hardware products and greater variety than the NHS but Meta products remained the most popular followed by HTC and Pico products. 11 also selected ‘other’ which included an onsite and streaming CAVEs.

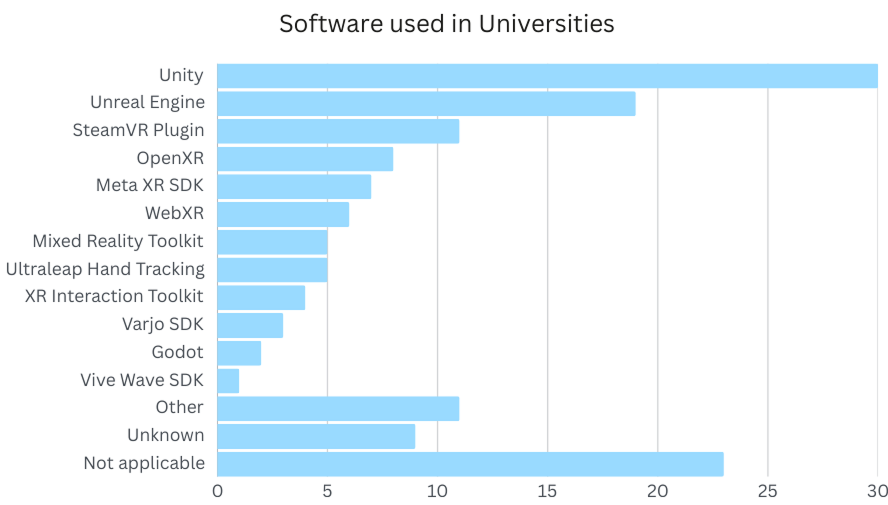

With the greater number of respondents developing XR technology, more software is being used by universities. Unity was the most popular, followed by Unreal Engine and SteamVR Plugin.

Private sector companies

Data from private companies deploying XR technologies was collected using an AI chatbot assisted survey (see Research Methodology). By the 2nd September, 36 different companies had filled out this survey (accounting for duplicate responses) providing details of their company, XR technology, which disorders and populations their technology covers and what challenges they have faced among other details. The majority of these companies work across mental health, due to the Mindset XR funding initiative that has supported particularly mental health projects.

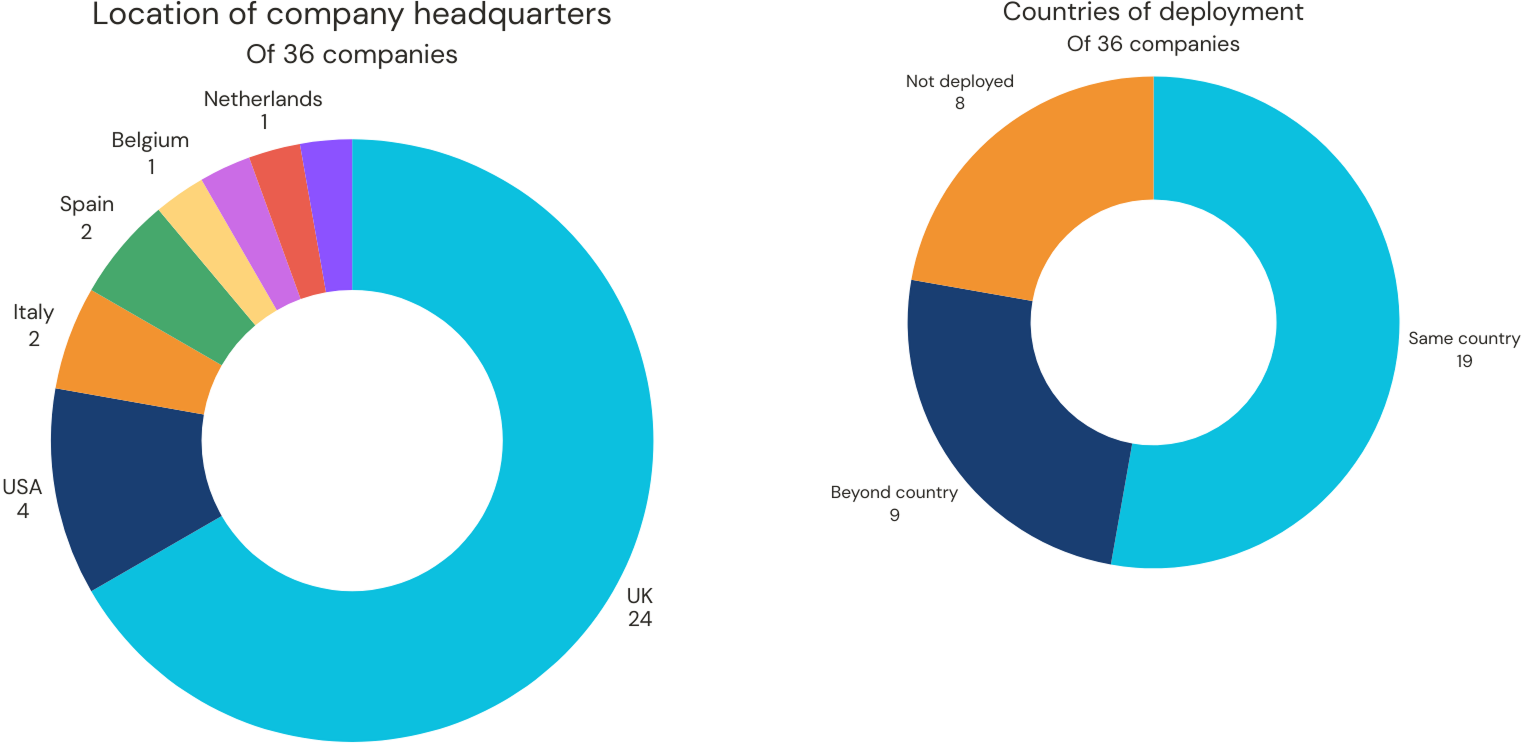

Of these 36 companies, the majority (24) had their company headquarters located in the United Kingdom but other headquarter locations included the USA (4), Italy (2), Spain (2), Belgium (1), the Netherlands (1), Poland (1) and Ireland (1).

Of these companies, 8 had not yet deployed their XR products. Meanwhile, 19 had deployed them exclusively within the same country as their headquarters, with 9 deploying outside of their headquarter’s country; including the EU (e.g. Germany, Belgium, the Netherlands, France, Poland, Sweden), North America (e.g. USA, Canada) and some reporting worldwide deployment including Australia, South East Asia, New Zealand.

Of 36 companies

Of 36 companies

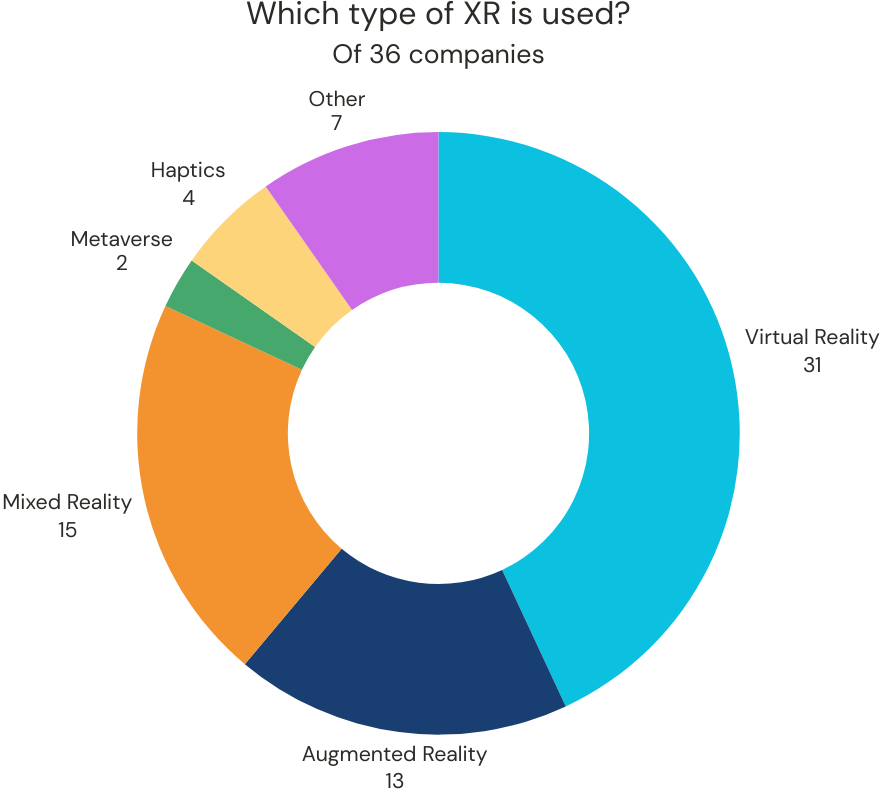

When asked which type of XR technologies the companies were using for their products, the majority of companies in the survey reported using virtual reality (n=31). However, companies were able to select multiple options, with 15 companies using augmented reality, 15 using mixed reality, 2 using metaverse, 4 using haptics and 7 selecting ‘other’. Of these, 12 companies indicated only using one type of these technologies while the remaining 24 reported using multiple different XR technologies.

Of 36 companies

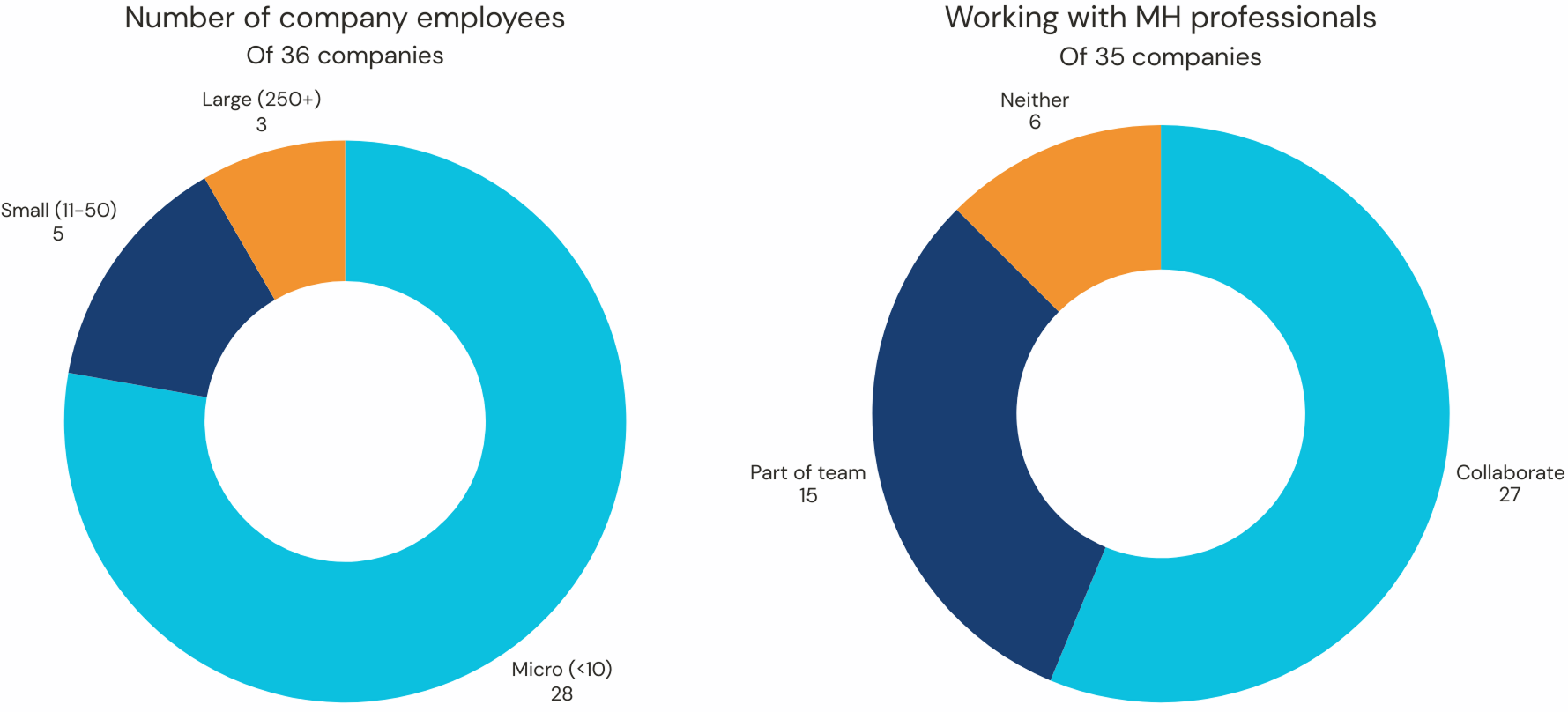

The majority of companies who responded to our survey were micro companies, with less than 10 employees (n=28) and typically collaborate with mental health professionals (n=27) with many also reporting to have mental health professionals embedded within their team (n=15). Six companies reported that they had not worked with mental health professionals. The market appears still nascent in terms of the size of the companies occupying the space. Therefore, early movers into the space are likely to benefit from an open market which they can scale rapidly into.

Of 36 companies

Of 35 companies

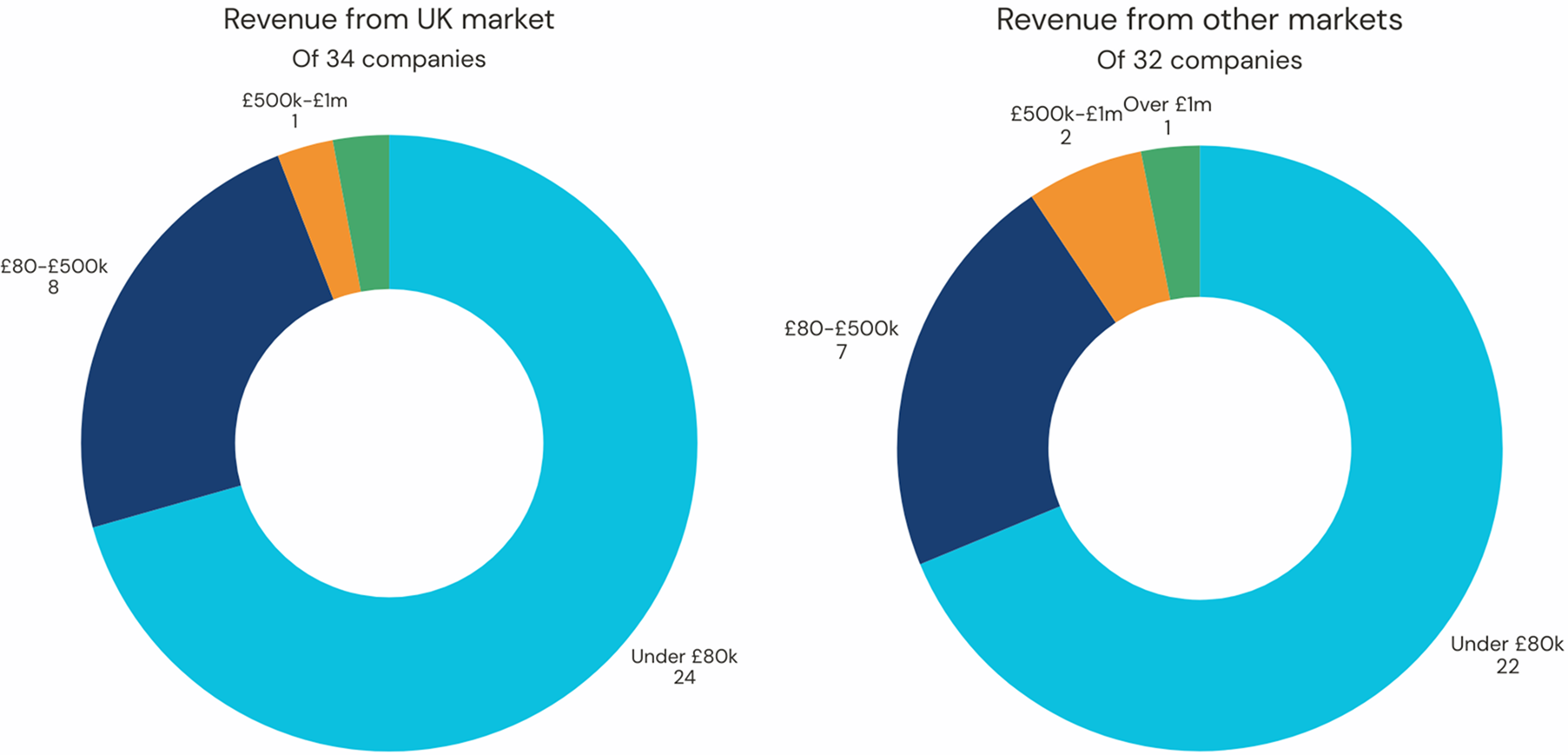

Only one company reported that their UK revenue was over £1 million with the majority reporting under £80k (n=24). This was similar to the revenue from other markets.

Of 34 companies

Of 32 companies

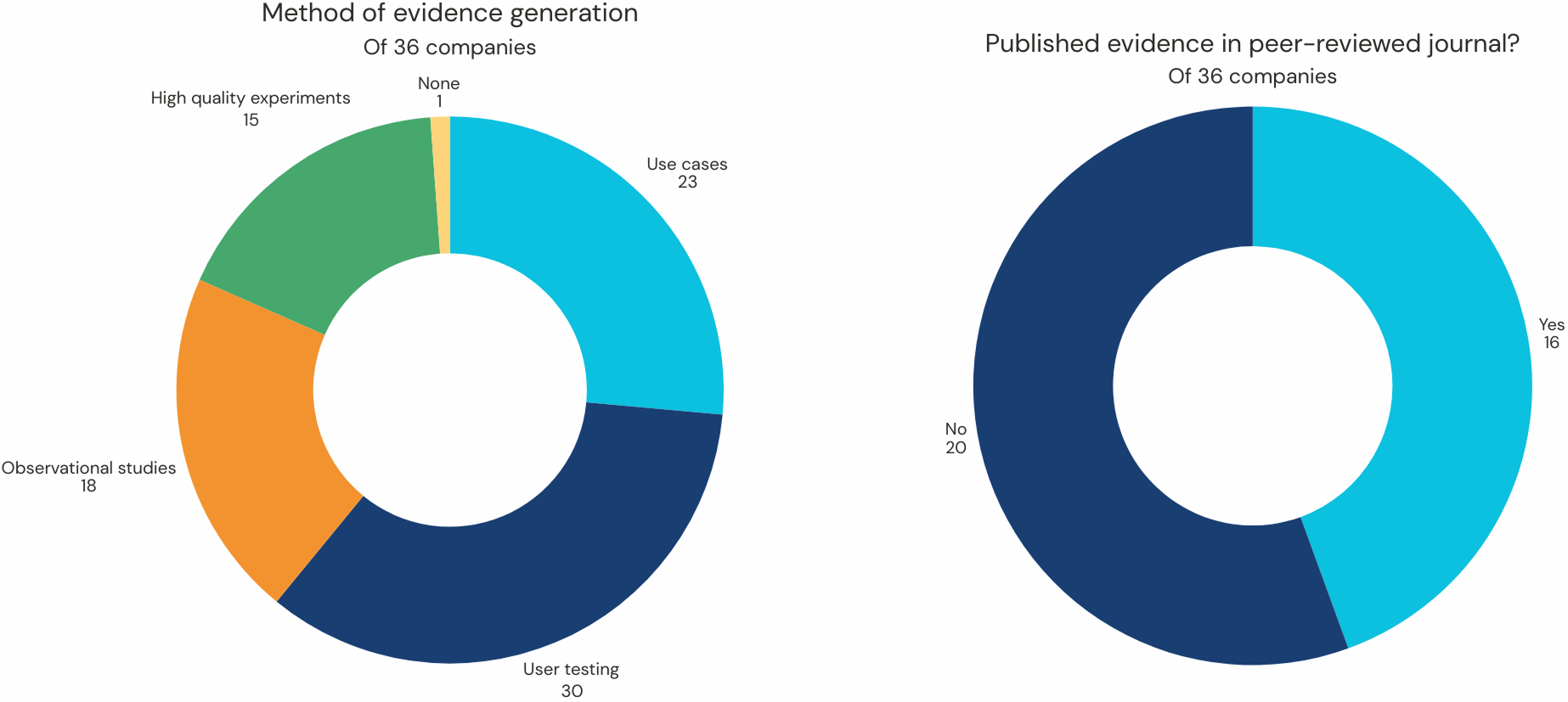

Evidence is mainly being generated through user testing (n=30) and use cases (n=23) with 15 reporting that they had conducted high quality experiments and 16 reporting that evidence had been published in a peer-reviewed journal. Only one company reported that they had not yet generated evidence.

Of 36 companies

Of 36 companies

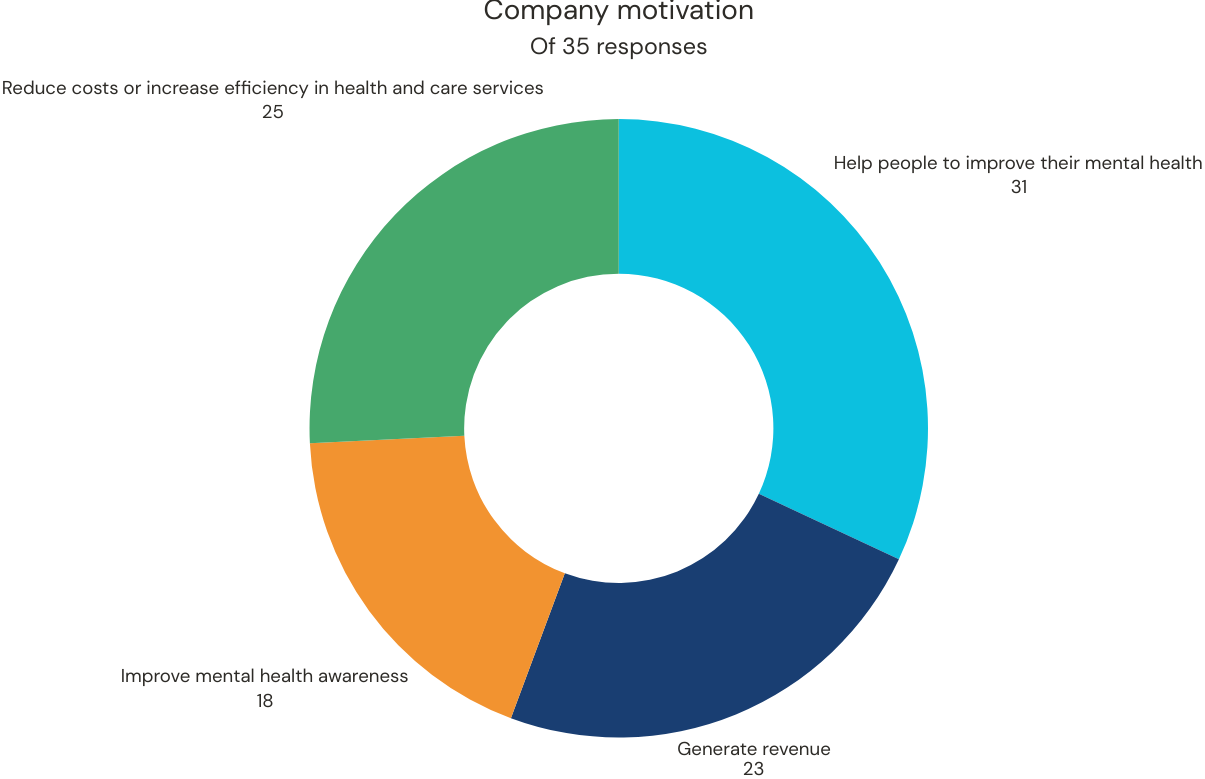

Companies were asked their motivation for developing XR technologies. Most companies selected multiple answers but answers were split between helping people with their mental health (31), generating revenue (23), improving mental health awareness (18) and reducing costs and improving efficiency in services (25).

Of 35 responses

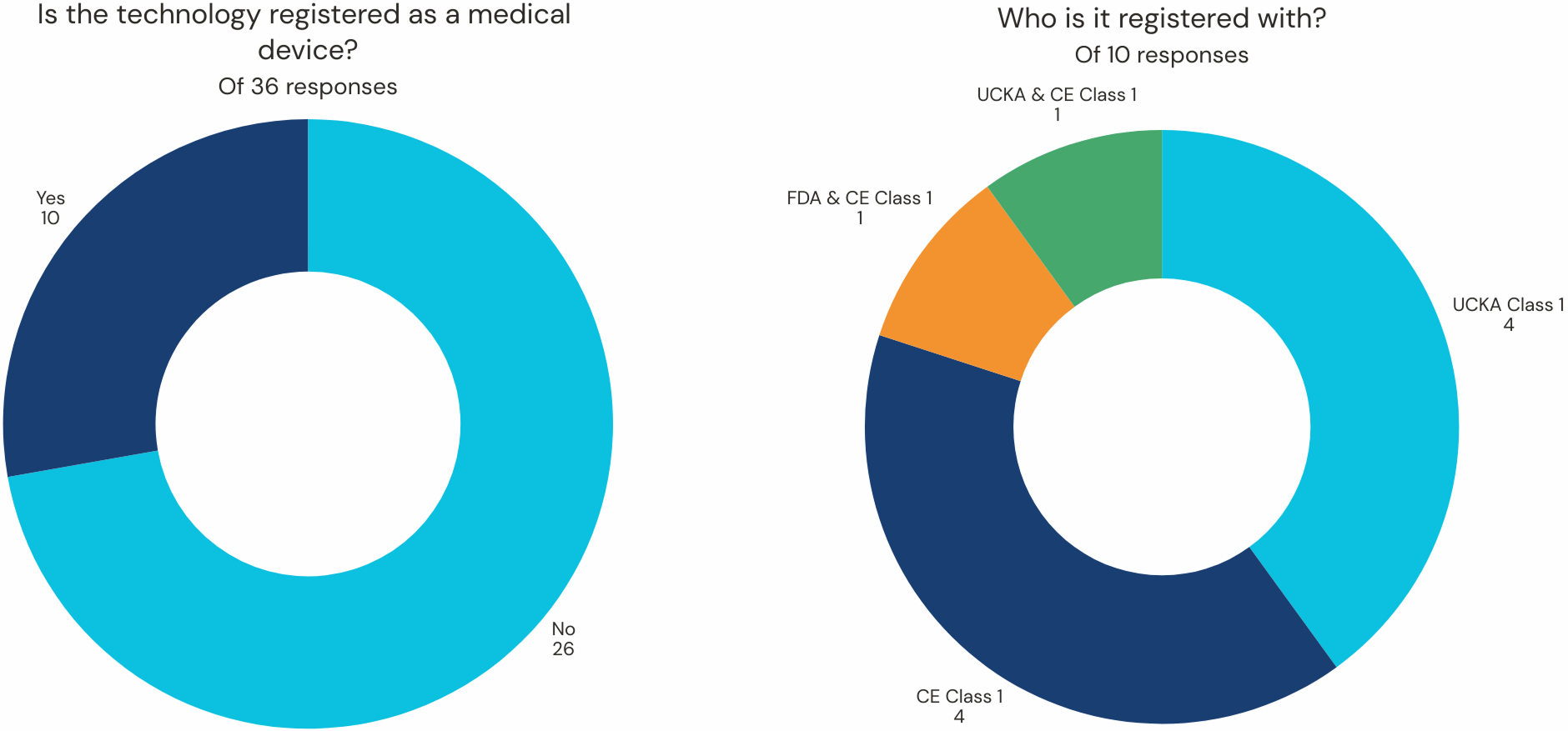

The majority of companies have not registered their products as software as a medical device (n=26) but of the 10 that have, four are registered in the UK, four in the EU with one being registered in both the US and EU and the final one being UK and EU registered.

Of 36 responses

Of 10 responses

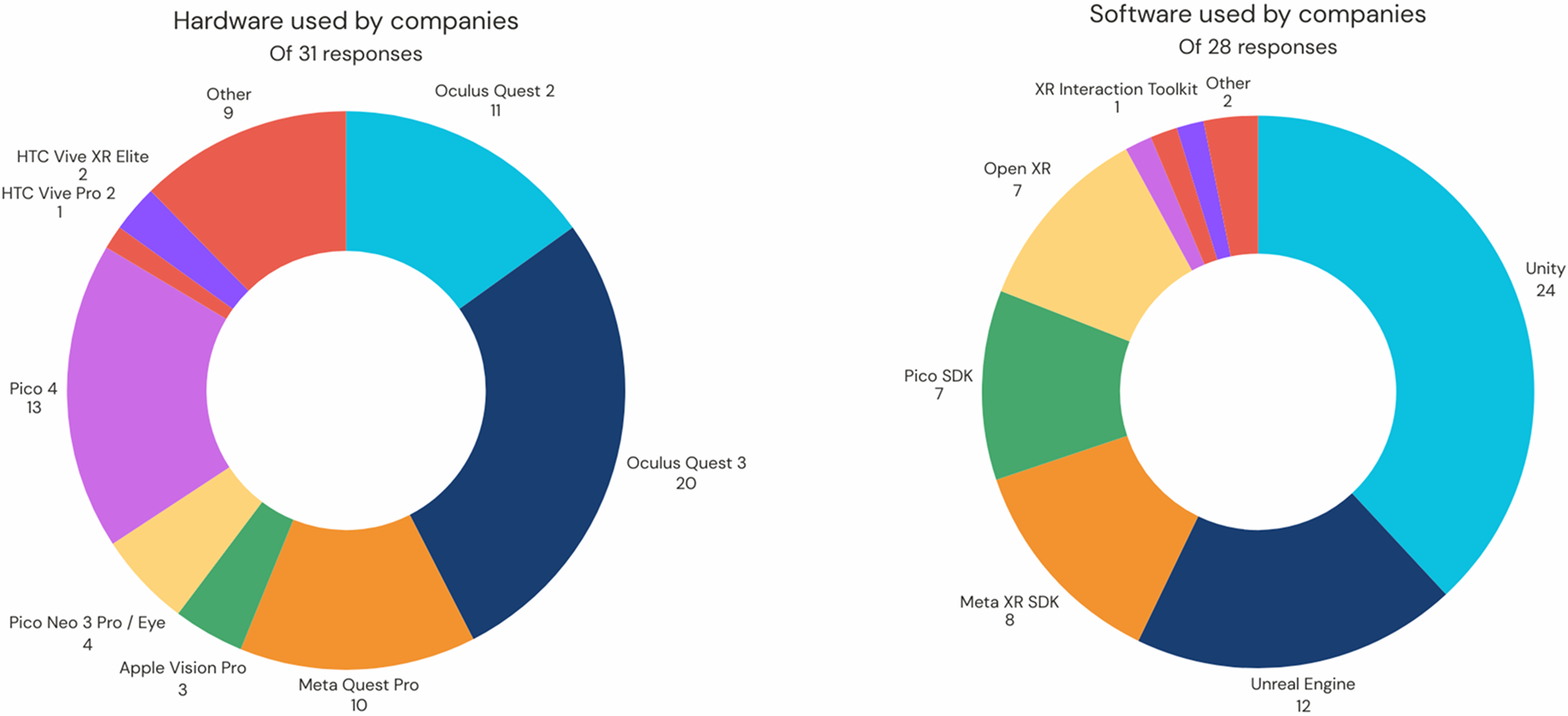

Meta Quest products were still most popular amongst companies, similar to the NHS and universities, particularly the Meta Quest 2 and 3 headsets. However, Pico, Apple and HTC products were also used. Similarly, Unity and Unreal Engine were also the most popular software.

Of 31 responses

Of 28 responses

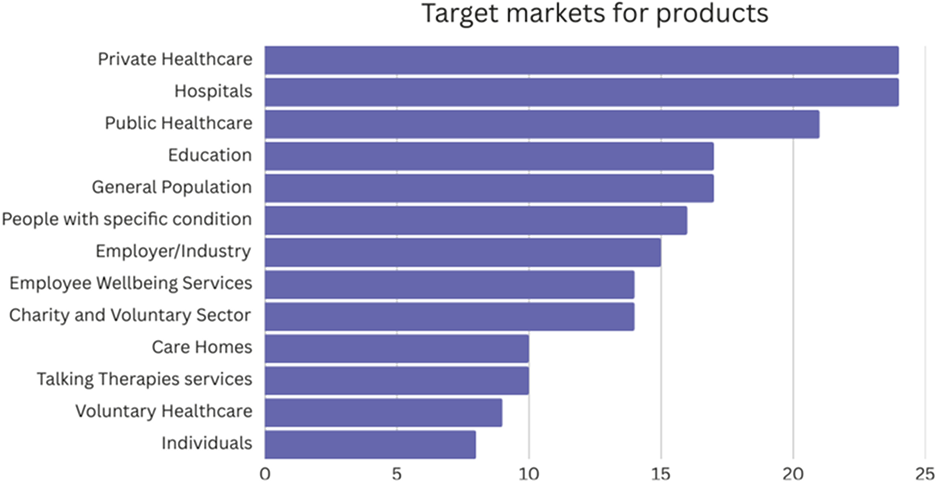

Populations and target markets

To understand the target markets and populations for XR companies, they were asked 1) who they market their products to, and 2) to describe who the end-user of their products are and the specific organisations who may use it.

As shown in the graph, almost all companies market to healthcare venues, both private and public, including hospitals, NHS Trusts and Talking Therapy services. Many also market their products for educational purposes, such as to universities for medical or nursing students with other companies also marketing to the third sector and social care (including charities, care homes, voluntary healthcare), to employers (such as Employee Assistance Programs and workplace wellbeing initiatives) and some directly to consumers (general population, individuals, those with specific conditions).

End-users and organisations were described by each company and included:

- Mental health and healthcare professionals (including those in Talking Therapies, private healthcare, NHS Trusts, occupational health)

- Researchers and universities (including those with XR labs and research students)

- Care homes and workers (including psychologists, activity coordinators, care therapists)

- Direct to individuals (also referred to as patients, service users and/ or clients)

- Other therapists including art therapists and coaches

- Educators of medical and nursing students

- General population and those with specific mental health conditions such as depression or anxiety (direct to consumer)

- Specific population groups such as young people, marginalised groups, those with specific conditions.

- Employers for employee wellbeing services, workplace settings, HR

- Charities and voluntary sector organisations

Conditions

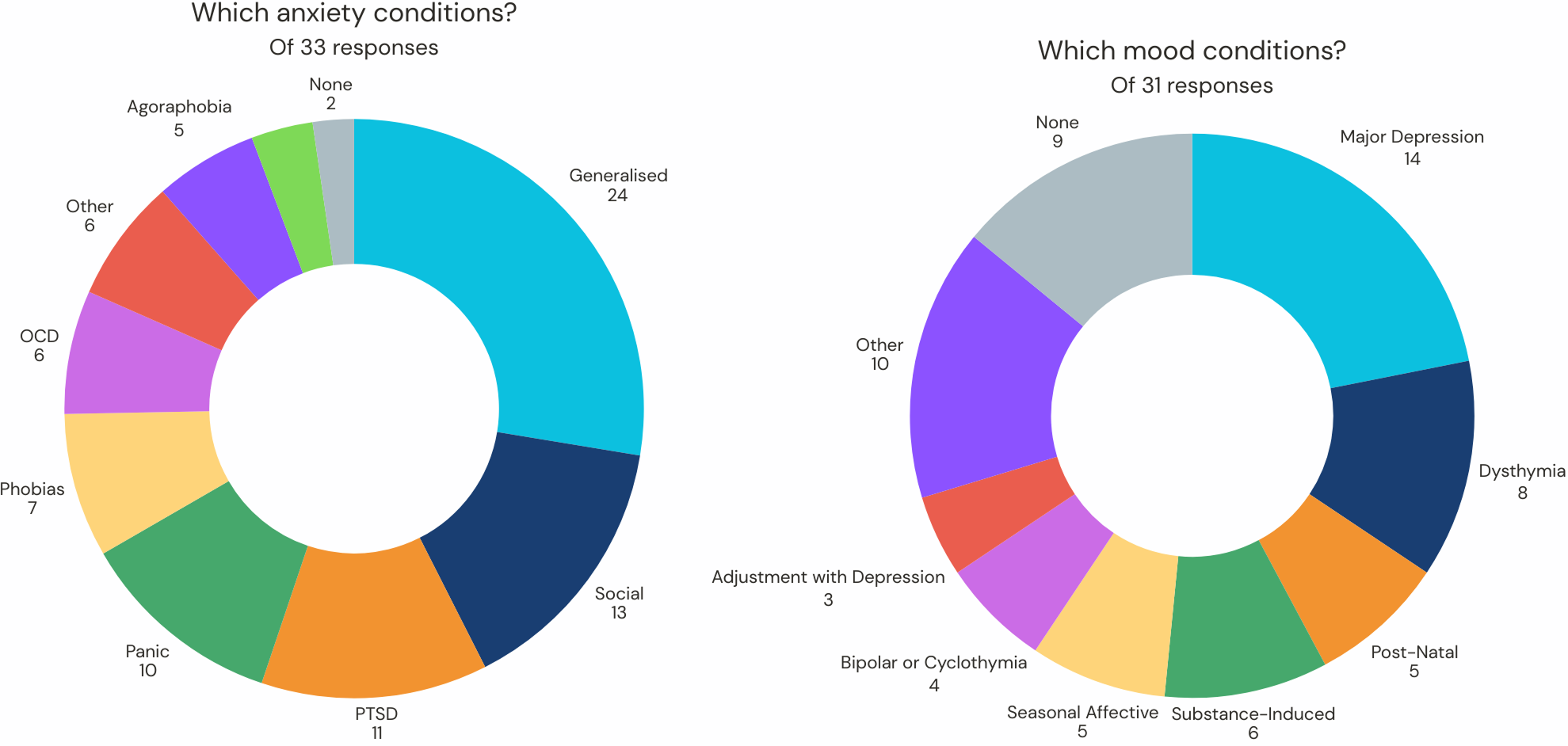

Anxiety (n=31) and depression (n=22) are the most common mental health conditions that companies targeted with their XR products. The most common anxiety conditions targeted are generalised and social anxiety, with some companies also covering post-traumatic stress disorder (PTSD), panic disorder, phobias, obsessive-compulsive disorders and other anxiety conditions. Similarly, whilst major depression, dysthymia and “other” were targeted the most by companies, adjustment disorder, substance induced mood disorder and bipolar were the least covered.

Of 33 responses

Of 31 responses

One company reported that they targeted all disorders but also indicated that they are developers employed by others to make products - this suggests that not all companies are already equipped with the clinical knowledge but feel confident that their skills can be applied in all areas of mental health.

Other conditions that were covered by companies include eating disorders such as anorexia or binge-eating disorder (n=5), psychotic disorders such as schizophrenia and psychosis (n=5), neurodegenerative diseases such as Alzheimer’s and Motor Neurone Disease (n=8), cognitive-related conditions such as Vascular or Lewy Body dementia (n=3). Other conditions reported included stroke (n=6), traumatic brain injuries (n=5), epilepsy, brain tumours and multiple sclerosis (n=3). Most companies reported covering more than one condition.

Companies in this survey were also asked about the challenges they have experienced and where they see future opportunities for XR technologies. These are reported in the Challenges and Opportunities section of this report.

Market trends, growth potential, and investment opportunities.

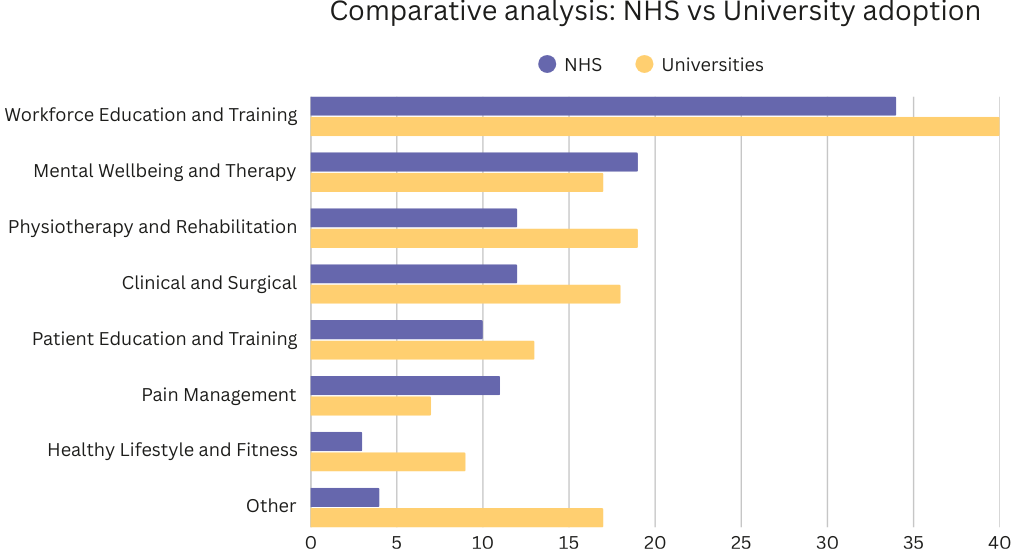

Our Freedom of Information requests to NHS Trusts and UK universities revealed consistent patterns of how immersive technologies are being deployed across the healthcare ecosystem.

The data shows five primary application categories with varying levels of implementation and adoption between clinical and application settings:

74

Workforce Education and Training Sites

36

Mental Wellbeing and Therapy Sites

31

Physiotherapy and Rehabilitation Sites

30

Clinical and Surgical Sites

23

Patient Education and Communication Sites

This distribution demonstrates that while workforce training dominates current applications, significant investment is also being directed into rehabilitation and therapeutic interventions. These findings suggest that UK healthcare institutes are beginning to embrace immersive across education and clinical domains, but universities are leading adoption of XR technologies, primarily for research and development (R&D) or student education, compared to NHS Trusts.

Workforce Education and Training

With 74 total implementations (NHS n=34, universities n=40), workforce education and training represents the most substantial application area for XR technologies in UK healthcare settings. Universities are leading this adoption, leveraging immersive environments to revolutionise how healthcare professionals, such as medical and nursing students, are trained. It is important to highlight here that another 17 universities reported ‘other’ categories of adoption. This primarily was explained to be for student education and training, showing an even greater use of XR technologies in the training of current and future healthcare professionals. This is perhaps unsurprising given one of the key functions of universities is for student education, but universities also engage heavily in research and development (R&D) and this is highlighted in how universities are more likely to be researching XR technologies than NHS sites.

The applications primarily focus on three key domains:

- Clinical simulation training in controlled, repeatable virtual environments

- Soft skills development, including communication, empathy, and patient interaction

- Process-driven tasks and procedural training for standardised care delivery

This widespread adoption reflects the significant advantages of immersive learning: reduced training costs, elimination of patient risk, standardised educational experiences, and the ability to practice rare or high-risk scenarios repeatedly until competency is achieved.

The University implementations suggest that XR technologies are being integrated into curriculum development and research initiatives before transitioning to clinical settings, potentially creating a pipeline of healthcare professionals already familiar with immersive training methods before entering NHS employment. High numbers within the NHS also suggest that XR technologies are playing a role within training in-situ, demonstrating their value in education but also opportunities for healthcare professionals to improve digital literacy.

Mental Wellbeing and Therapy

With 36 total implementations (NHS n=19, universities n=17), mental health and wellbeing highlight a significant area of growth for VR/AR applications in UK healthcare. As shown by the data collected from XR companies, the majority of these products may focus on depression and anxiety conditions but extend beyond this into other complex conditions such as Alzheimer’s, dementia, eating disorders and psychotic disorders.

Anxiety Treatment

Virtual environments allow patients to confront anxiety-inducing situations in controlled settings, with therapist guidance and adjustable intensity levels. This form of exposure therapy shows particular promise for specific phobias and social anxiety disorder. The majority of treatments tend to appear within B2B and healthcare contexts, however, there is an increasing interest in B2C interventions. These include fear of heights and fear of public simulations that are being launched on online platforms for usage at home.

Cognitive Behavioural Therapy (CBT)

XR-enhanced CBT creates interactive scenarios for patients to practise cognitive restructuring and behavioural techniques in realistic situations, providing immediate feedback and reinforcement of therapeutic principles. A lack of an evidence base and the time and expense of the medical device regulation (MDR) classification pathway has resulted in a dearth of CBT for treatment offers so far (a similar picture exists in the Artificial Intelligence CBT space currently also). Therefore, until the pioneers in this space further develop a larger evidence base, therapy either direct to patients or facilitated by a healthcare professional within the NHS, will struggle to scale at pace. Investment support to develop evidence and XR specific regulatory development is critical to bridge this barrier.

Mindfulness and Relaxation

Immersive natural environments and guided meditation experiences are being deployed for stress reduction, pain management, and general wellbeing support, offering multi-sensory engagement that enhances traditional relaxation techniques. In many cases, the new MHRA guidance would suggest that these types of XR technologies may not classify as a software as a medical device, suggesting a market for non-clinical wellbeing tools.

Given the balanced adoption across clinical and academic settings, this equal distribution suggests that mental wellbeing applications have successfully bridged the research-to-practice gap, with effective knowledge transfer between universities and NHS mental health services. UK researchers are particularly focused on evaluating long-term efficacy and identifying which patient populations benefit most from these immersive therapeutic approaches, with several large-scale clinical trials currently underway across the country.

Physiotherapy and Rehabilitation

With 31 total implementations (NHS n=12, universities n=19), physiotherapy and rehabilitation represents an important area for VR/AR applications in UK healthcare. Academic institutions are leading research and development, with data to suggest that promising innovations are successfully transitioning to clinical practice.

The primary focus areas include:

- Stroke rehabilitation, particularly for upper limb function recovery

- Neurorehabilitation for traumatic brain injury and neurological conditions

- Movement re-education and gait training

- Gamified therapy approaches to increase patient engagement and adherence.

These applications leverage the motivational aspects of immersive environments, addressing a critical challenge in rehabilitation: patient engagement with repetitive exercises. By transforming necessary repetitions into engaging activities with immediate feedback, VR/AR technologies are demonstrating improved compliance and potentially accelerated recovery trajectories.

UK research centres are particularly focused on developing adaptive systems that automatically adjust difficulty based on patient performance, creating personalised rehabilitation programmes that evolve with the patient’s recovery journey. NHS Trusts are now evaluating these systems for potential wider implementation across rehabilitation services but not in a systematic manner. Further research funding (outside of the Mindset XR Programme which concentrates solely on mental health) is necessary to develop the evidence for this and other healthcare verticals, particularly research that can demonstrate not only improved outcomes but cost-effectiveness.

Clinical and Surgical Training

With 30 total implementations (NHS n=12, universities n=18), clinical and surgical training represents a specialised but high-impact application area for immersive technologies in UK healthcare settings. This is separate to Workforce Education and Training, as it offers insight into direct clinical practice, where XR can support surgeons and clinicians in direct applications and preparing for complex procedures and surgeries.

Surgical Simulation

Advanced haptic feedback systems paired with VR provide realistic surgical training environments where trainees can practice complex procedures repeatedly without patient risk. These systems are particularly valuable for laparoscopic and robotic surgery training, where depth perception and spatial awareness are critical skills. Such systems and applications are also deployed for soft skills required for healthcare staff, as discussed in Workforce Education and Training.

Anatomical Exploration

AR applications allow trainees to visualise and interact with detailed 3D anatomical models, either overlaid on mannequins or floating in space. These applications enable understanding of spatial relationships between structures that traditional 2D learning materials cannot provide.

Rare Case Preparation

VR environments allow surgical teams to prepare for complex or unusual cases by practising on virtual models created from actual patient imaging data. This patient-specific rehearsal can identify potential complications before the actual procedure, improving surgical outcomes.

The balanced distribution between NHS and university implementations suggests strong collaboration between academic and clinical institutions in this domain, with innovations rapidly transitioning from research to practice. Royal Colleges are increasingly incorporating VR assessment into specialist training programmes, signalling growing acceptance of these technologies as valid educational tools.

Patient Education and Communication

With 23 total implementations (NHS n=10, universities n=13), patient education and communication represents a small but potentially transformative application area for immersive technologies in UK healthcare. These applications directly address the challenge of health literacy and patient engagement with their own care.

Key applications include:

- Pre-procedure orientation and anxiety reduction

- Condition-specific educational experiences

- Treatment plan visualisation and understanding

- Hospital onboarding and navigation assistance

By creating immersive explanations of complex medical concepts, these applications help patients better understand their conditions and treatment options, potentially improving informed consent processes and treatment adherence.

Early research from UK universities suggests that VR-based patient education may be particularly effective for populations with lower health literacy or language barriers, as visual and experiential learning can transcend some communication challenges. Several NHS trusts are now piloting these approaches in pre-operative clinics and chronic disease management programmes.

Comparative Analysis: NHS vs University Adoption

Our comparative analysis reveals several important patterns in VR/AR adoption across the UK healthcare ecosystem:

- Academic Leadership: Universities consistently show higher implementation rates across all application areas, highlighting their role as innovation drivers in healthcare technology.

- Deployment: Responses from healthcare services demonstrate that XR technologies in the NHS are primarily used at NHS sites by staff and patients, as opposed to home use. This will vary based on service and use, but there is greater potential for home use by patients, as highlighted by our case study on Tend.

- Translation Gap: The difference between university and NHS adoption rates indicates opportunities to improve knowledge transfer and technology translation pathways, while acknowledging the different functions of healthcare organisations versus universities and how this plays out when it comes to implementation.

- Mental Health Parity: Mental wellbeing applications show equal adoption across both sectors, suggesting particularly effective research-to-practice translation in this domain. But, this is difficult to corroborate with the limited number of sites currently offering mental health solutions/trials.

- Implementation Barriers: The lower NHS adoption rates likely reflect institutional barriers including funding constraints, technical infrastructure limitations, and staff training requirements.

- Student Education: As education institutes, universities’ primary goal is the education of students and this is demonstrated through the selection of ‘other’ adoption methods reported here in the data. This ‘other’ was importantly shown to be XR being used in student education, for example for medical or nursing students, or for student research projects, highlighting a key difference between healthcare and universities use of XR.

These findings suggest that while promising research is abundant, more structured pathways for implementing proven VR/AR solutions into routine clinical practice are needed to fully realise their potential benefits within the NHS.

Market Growth and Statistics

The global XR healthcare market has experienced explosive growth, with the market valued at £3.54 billion in 2024 and projected to reach £35.16 billion by 2033, representing a remarkable compound annual growth rate (CAGR) of 29.04%. Multiple research firms report similar trajectories, with some forecasting the market will hit £16.83 billion by 2034 at a CAGR of 24.81% [11].

The pandemic has permanently shifted healthcare’s relationship with digital technologies. In February 2025, XRHealth acquired RealizedCare, solidifying its position as the largest AI-driven therapeutic XR platform worldwide [12]. This reflects the maturing ecosystem where major players like CAE Healthcare, GE Healthcare, and Microsoft are leading innovation, with recent developments including Apple’s Vision Pro launch in March 2024 seeking to transform healthcare sectors including clinical education, surgical planning, and behavioural health.

North America dominates the global XR healthcare market with 41% market share in 2024, driven by strong R&D investments and government support [13]. However, Asia Pacific is estimated to grow rapidly during the forecast period, contributing more than 40% of the rise in global healthcare spending [14]. The UK leads global initiatives to scale government led programmes for XR Health in the form of Mindset XR [15] which aims to grow the UK’s nascent immersive digital mental health sector by investing in projects which deliver immersive digital mental health therapeutics and creating a supportive ecosystem which will help companies bring these innovations to market. Whilst the majority of companies surveyed appear to be focussed on B2B, increasingly more B2C offerings are being launched. A number of wellbeing and fitness products have been successfully launched on headsets, due to hardware companies concerned about what is classified as software as a medical device there have been limitations. However, headsets such as the HTC Vive Flow focussed predominantly on wellbeing applications, launching with products including Healium, Explore Deep and Tripp.

Emerging Trends and Investment Opportunities

1. AI-Enhanced Personalisation

One of the most exciting frontiers for XR in healthcare is the integration of artificial intelligence and to personalise experiences in real time. For example, Emteq: originally a biofeedback embedded VR headset company, they have pivoted to smart glasses. Their current offerings include the OCOsense™ smart glasses developed by Emteq Labs. Optomyography technology embedded within their glasses now tracks chewing cycles and eating patterns in real time. Combining machine learning and biofeedback with haptic feedback their glasses help reduce chewing rate. Initial results demonstrated that haptic feedback may reduce chewing rate, and ultimately modifying eating behaviour to reduce obesity [23]. These systems create “closed-loop” feedback environments, where users’ states influence the XR environment, enabling dynamic, adaptive care that can respond to the needs of each individual. AI personalisation is increasingly being combined with additional input and feedback, however, there is a need to consider the safety and regulation of such AI-assisted technologies.

2. Biofeedback and Mind-Body Applications

The role of biofeedback across recovery has been a known approach for many years. Researchers such as Diane Gromala demonstrated research that shows the role of biofeedback as a tool for reducing pain as early as 2015 [24]. Research increasingly demonstrates the importance of the connection between emotional and physical health, and the role of interoceptive awareness in trauma recovery. New innovations that link embodiment and physiological visualisation to trauma are showing increased value in supporting anxiety regulation. For example, Explore Deep uses meditation in VR guided by breathing sensors to reduce anxiety and support emotional regulation [25]. SOUL PAINT, for example, is a multisensory experience designed to support emotional expression and trauma recovery through enabling patients to visualise the complex interplay of emotion and sensation to enhance interoceptive awareness and support stakeholder communication [18]. XR platforms are increasingly interpreting, visualising and adapting to a user’s emotional or physical state by analysing signals such as heart rate, gaze, or body movement.

3. XR for At-Home Care and Remote Access

With the rise of affordable, standalone headsets, XR healthcare experiences are no longer confined to hospital or clinic settings. Increasingly, experiences are being designed for home use, supporting rehabilitation, mental health, and wellbeing remotely. Examples include Concept Health Technologies, which offers physiotherapy and pain management VR programs, was one of the only ways that COPD rehabilitation continued during the pandemic in the UK [1]. International examples include XRHealth, which connects patients to remote therapists through a VR platform for at home use [26]. This decentralised approach offers greater access to care, particularly for those in rural, coastal or underserved areas but also demands new models of safeguarding, digital inclusion, and remote monitoring. However, our findings from the NHS suggest deployment for home use remains limited.

4. Medical and Clinical Education

Medical education remains one of the most widely adopted use cases for XR in healthcare. Immersive simulation environments allow students and professionals to train in high-pressure scenarios without risk. This includes procedural training, emergency response, anatomy, soft skills, and empathy development. The NHS England Technology Enhanced Learning (TEL) team has been at the forefront of this movement, developing training programmes across NHS Trusts. Tools like FundamentalXR [27] and Oxford Medical Simulation [28] allow for repeated practice of surgical procedures, while also building emotional readiness. Dr. Abison Logeswaran’s research has been pivotal in creating evaluation protocols that ensure these tools meet rigorous pedagogical standards [29]. Meanwhile, Bodyswaps [41] uses VR and AI for training and roleplay in interpersonal communication, teamwork, conflict management and empathetic care. Education of both students and healthcare staff remains one of the most applicable areas for XR technology in the UK in the NHS and academia.

5. Neurodivergence and Sensory Environments

A growing focus in XR healthcare is inclusive and accessible design, ensuring that experiences can be used by people with diverse physical, cognitive, and sensory needs. Tailored XR interventions are now being used for stroke recovery, dementia care, and neurodivergent users. REMO Health offers VR cognitive training for people with dementia, while other startups are creating sensory-friendly environments for neurodivergent users [30]. By working with communities and user researchers, these tools are becoming more adaptable, customisable, and empowering for a broader range of patients but more research is needed in this area.

6. Palliative and End-of-Life Care

An emerging application of XR in health is its use in palliative and end-of-life settings. Immersive environments can support pain distraction, spiritual reflection, and legacy-making, particularly for individuals facing life-limiting illnesses. Hospices such as Prospect House have developed tools such as Gardens of Serenity, combining pain management and anxiety reduction techniques for their patients. These interventions are deeply personal and underscore the power of immersive storytelling to support human dignity, agency, and connection at the end of life. Organisations such as End of Life Doula UK are actively experimenting within this space [31] but careful consideration of ethics and users remains crucial.

7. Psychedelic Research

There is growing global interest in the intersection of psychedelic therapies and immersive technologies. Institutions such as the University of California, San Francisco’s Neuroscape Lab, led by Dr. Adam Gazzaley, have been at the forefront of this movement, developing products that simulate altered states of consciousness. Gazzaley’s team has also contributed to the digital therapeutics landscape through ventures such as Akili Interactive, known for its FDA-approved video game for ADHD, and Sensync, a multisensory “immersion vessel” designed to induce meditative and psychedelic-like states.

Beyond academic institutions, several companies are actively exploring the potential of simulated psychedelic experiences. Notable examples include SoundSelf, Explore Deep, and Si-PHI (Simulated Psychedelic Immersive Experience), a new mixed reality intervention developed at Yale University. Si-PHI integrates biofeedback, including EEG and other physiological markers, to create adaptive therapeutic experiences. Early findings suggest that EEG patterns observed during Si-PHI sessions mirror those seen in ketamine-assisted therapy, indicating potential for non-pharmacological approaches to psychedelic healing.

This growing field is supported by a broader cultural and research ecosystem, including communities and events like the Cyberdelic Society, Awakened Futures Summit, Breaking Convention, and Consciousness Hacking, which have long championed the convergence of technology, consciousness exploration, and mental health innovation.

8. Creative Health

The creative health industry has seen significant growth in recent years, particularly since 2019. Over this period, several key institutions have been established to champion the integration of arts and health within communities, including the National Academy for Social Prescribing, the National Centre for Creative Health (NCCH), the Culture, Health and Wellbeing Alliance (CHWA), and the Arts Council England’s Creative Health team. These organisations have played a pivotal role in launching initiatives that embed creative practice within health and care systems.

In parallel, research and development in digital and immersive technologies for mental health has accelerated. A 2019 report by Nesta, in partnership with Sarah Ticho, titled The Role of Arts and Creative Practice in VR for Mental Health, helped catalyse new programmes at StoryFutures Academy, fostering collaborations between artists, SMEs, and researchers to explore XR and wellbeing. Audience insight guidance and a toolkit was also developed to support creative companies looking to create XR health and wellbeing solutions. Many of the projects supported through this initiative have since been further developed under the Mindset XR programme, which continues to drive innovation at the intersection of immersive technology and mental health.

More recently, in September 2025 the Creative Industries Council and Arts Council England released a new report titled CIC Health & Wellbeing Forum 2025 Report. The report sets out evidence and recommendations for strengthening initiatives that use creative and cultural activities, processes or assets to improve health and wellbeing for individuals and communities. This report includes reference to the role particularly of virtual reality, using the immersive arts and health experience Soul Paint as a case study. It finds that the programmes presented save the NHS money and argues they should play a critical role in the government’s efforts to shift the focus of healthcare systems away from a short-term reactive care model towards long-term health promotion, enabling more people to live well for longer.

Additionally, in 2025, a series of roundtables hosted at the Wellcome Trust and online titled p_ART_icipate! – Co-Creating Futures: Ethics and Policy Pathways for Participatory Digital Arts and Wellbeing brought together stakeholders to explore the ethical and policy dimensions of participatory creative health practices. Funded by the Arts and Humanities Research Council (AHRC) and led by a consortium including the University of Greenwich, Brunel University London, and the Central and North West London NHS Foundation Trust (CNWL), the p_ART_icipate! project is developing practical guidance for best practices in the design and delivery of participatory digital arts in health contexts. These resources are now being shared across cultural institutions, healthcare organisations, and artistic networks.

While still an emerging area, the integration of digital tools within social prescribing is gaining traction. Organisations such as NCCH, Arts Council England, and CHWA are increasingly focused on exploring how digital and immersive experiences can be meaningfully embedded within creative health pathways.

9. Paediatrics

In parallel with broader trends in creative health, there has been a rapid proliferation of applications focused on paediatric and youth populations—spanning prevention, intervention, and general wellbeing. Leading healthcare institutions such as Alder Hey Children’s Hospital, Sheffield Children’s Hospital, Glasgow Children’s Hospital, and Great Ormond Street Hospital have pioneered innovative approaches, from immersive rehabilitation programmes to the establishment of the first-ever Gamer in Residence role, integrating game-based interventions into patient care.

Further advancing the field, research consortiums such as CAHREL (Creative Arts, Health and Rehabilitation for the Early Life-course), led by Leeds Beckett University in collaboration with Leeds Teaching Hospitals NHS Trust, the University of Plymouth, Edge Hill University, and industry partner Xploro, are pushing the boundaries of arts-based healthcare research. Their work employs participatory, arts-led methodologies to drive innovation in healthcare delivery and is currently exploring new applications of immersive technologies to support children and young people across clinical and community settings.

Challenges and Future Outlook

Despite rapid growth, challenges across development and adoption remain. Models of how the digital literacy of healthcare workforces can be developed and how front-line staff can be actively involved in the design and development of creative digital interventions are lacking. Many studies on XR in healthcare education either poorly described or completely omitted their pedagogical approaches, with less than 3% of VR simulation papers incorporating a conceptual framework [16]. Companies and innovators continue to struggle to find clear routes to market, with limited paths for procurement - particularly within the NHS.

However, the XR healthcare community continues to gain interest and traction, and whilst adoption is slowly developing, the overall trajectory remains strongly positive. The UK is renowned for creating leading global innovators, both across the healthcare innovation arena, but equally across the creative industries and XR industry. This fusion of creative storytelling and game design is leading to powerful new innovations that enhance engagement, moving beyond gamification, supporting intrinsic motivation for patients to continue to engage in their rehabilitation. Immersive projects that have expanded from creative storytelling pieces into XR innovations such as Anagram’s Goliath and Impulse have won illustrious industry awards such as the Venice Biennale Grand Jury and Immersive Achievement Prize, and have recently received an Emmy nomination for Impulse [17]. Equally projects such as Soul Paint have gone onto win SXSW Special Jury Prize, Best Health and Wellness at Games for Change and other global recognitions for their potential across health and wellbeing, putting the UK XR industry on the map as a global innovator across healthcare and storytelling in XR [18].

The global AR and VR in healthcare market is projected to grow 30-35% from 2024 to 2029, driven by tech advancements, digitisation, government support, numerous start-ups, diverse applications, and increasing partnerships [19]. The XR healthcare market represents one of the most impactful use cases of early XR adoption in public services and industry, directly addressing some of the biggest global health challenges while improving access, a diversity of spaces for patients to engage, and ultimately creating scalable, cost-effective solutions for an increasingly strained healthcare system.